Each year, just in time for Christmas, the good folks at the Australian Bureau of Infrastructure, Transport, and Regional Economics (BITRE) publish a mountain of data in their Yearbook. This post aims to turn those numbers (and some other data sources) into useful knowledge – with a focus on vehicle kilometres travelled, passenger kilometres travelled, mode shares, car ownership, driver’s licence ownership, greenhouse gas emissions, and transport costs.

There are some interesting new patterns emerging – read on.

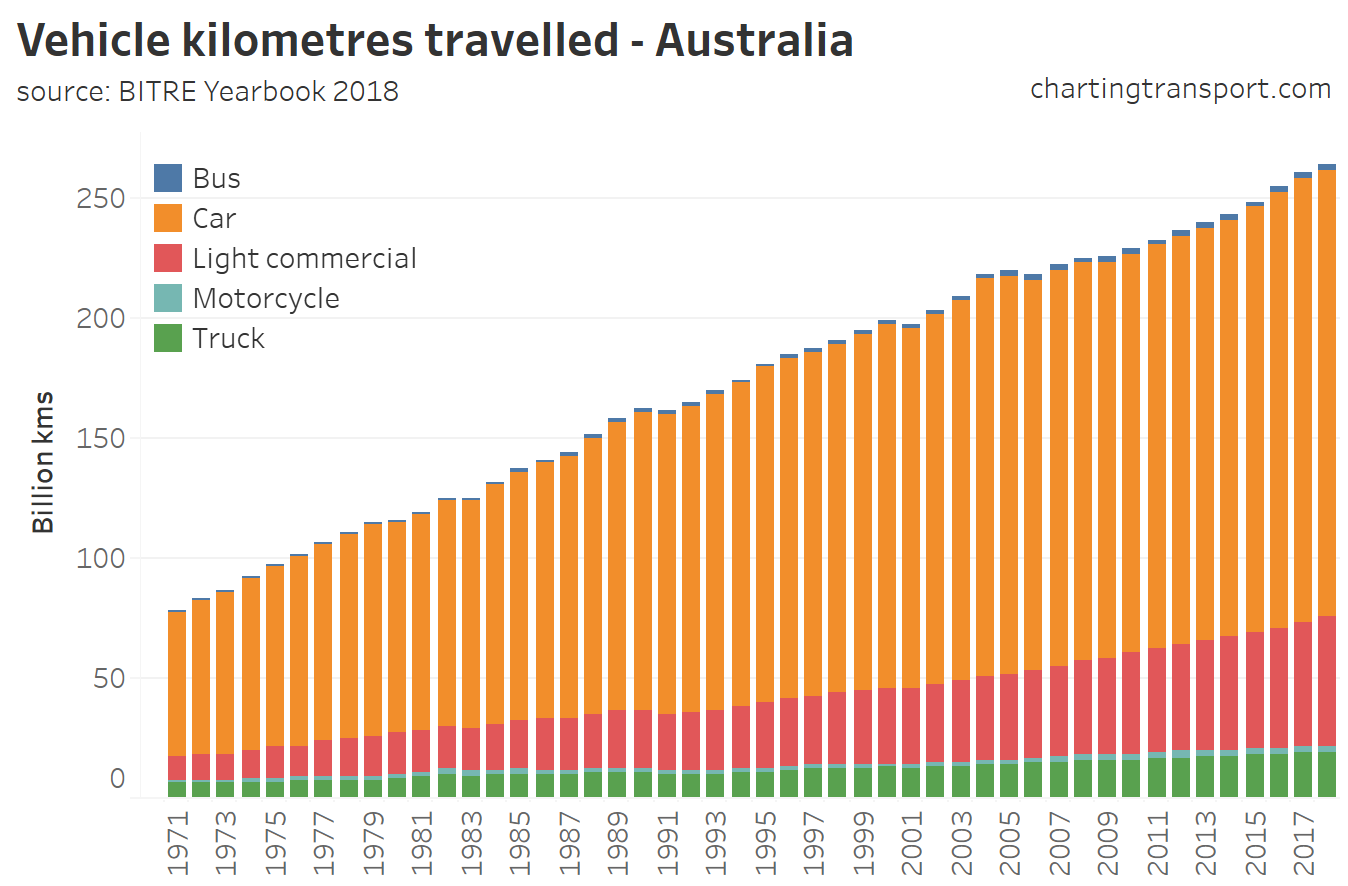

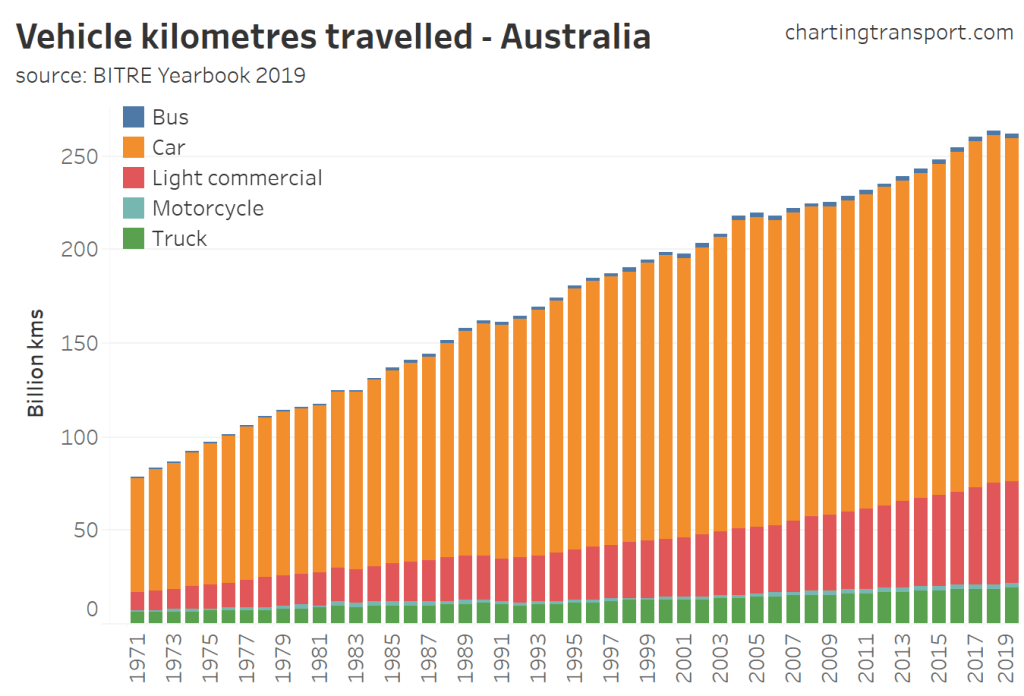

Vehicle kilometres travelled

According to the latest data, road transport volumes actually fell in 2018-19:

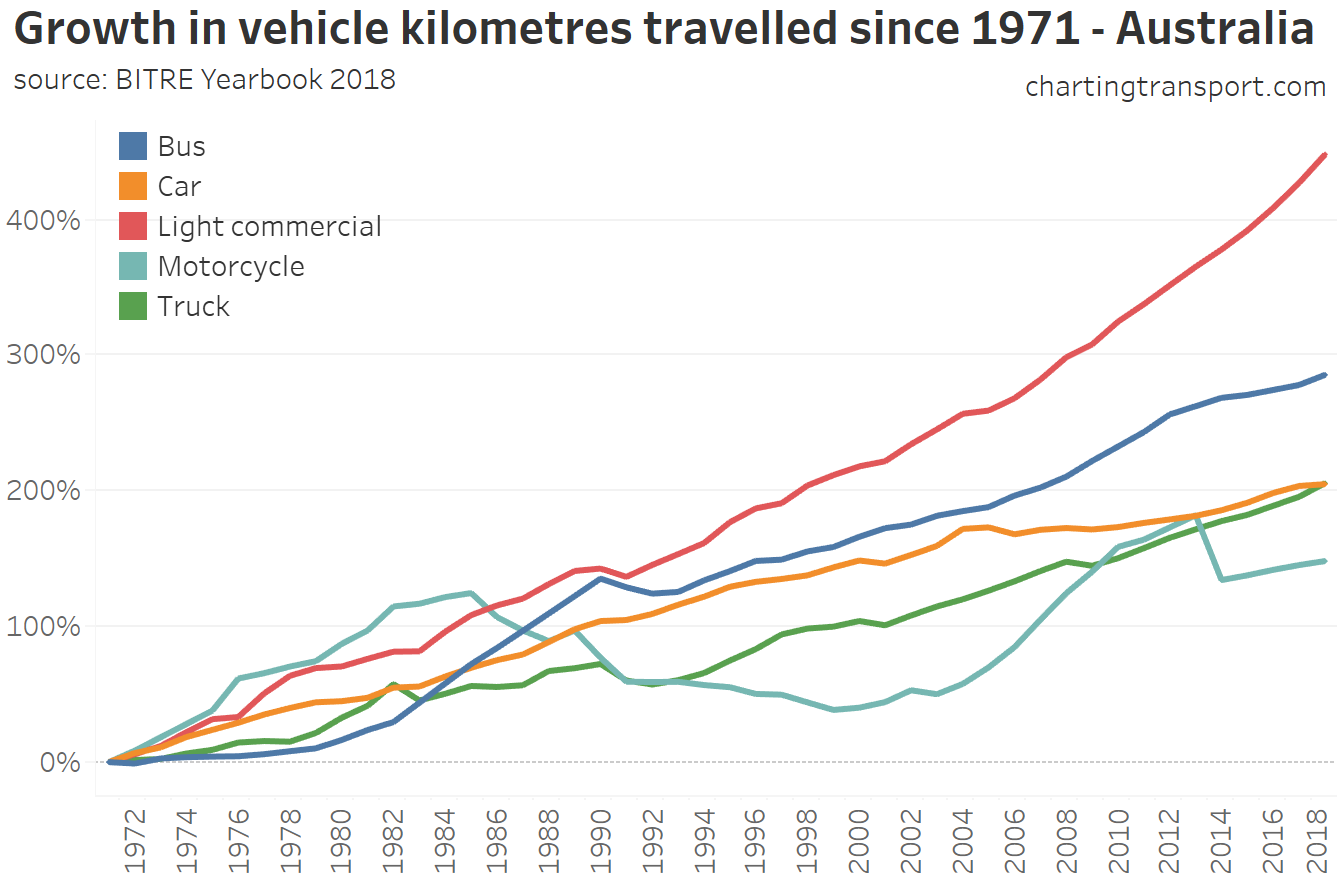

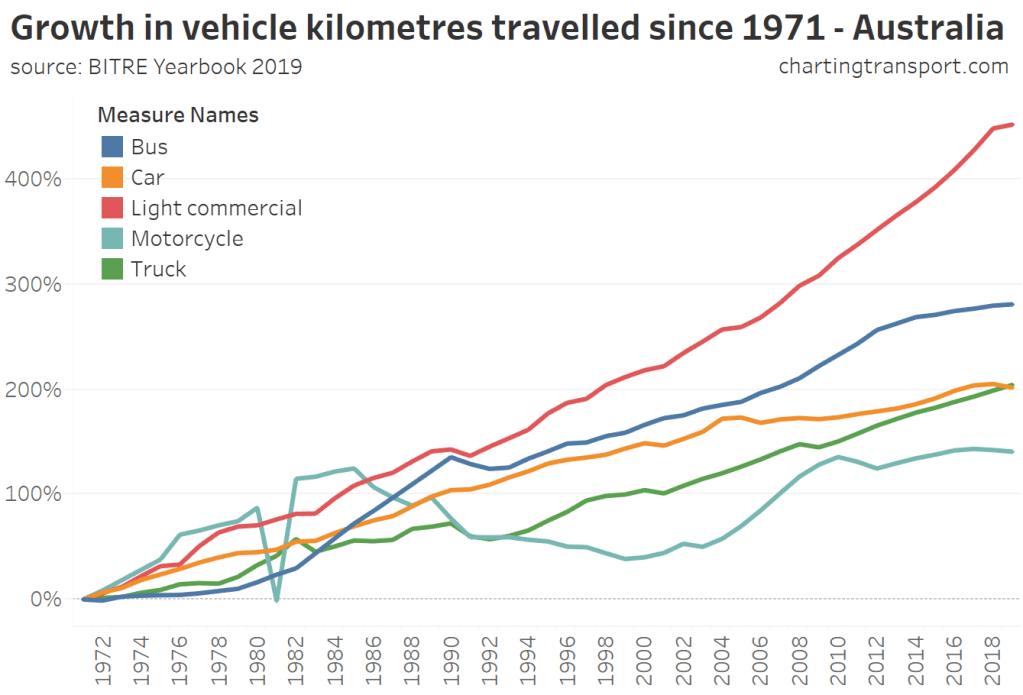

Here’s the growth by vehicle type since 1971:

Light commercial vehicle kilometres have grown the fastest, curiously followed by buses (although much of that growth was in the 1980s).

Car kilometre growth has slowed significantly since 2004, and actually went down in 2018-19 according to BITRE estimates (enough to result in a reduction in total vehicle kilometres travelled).

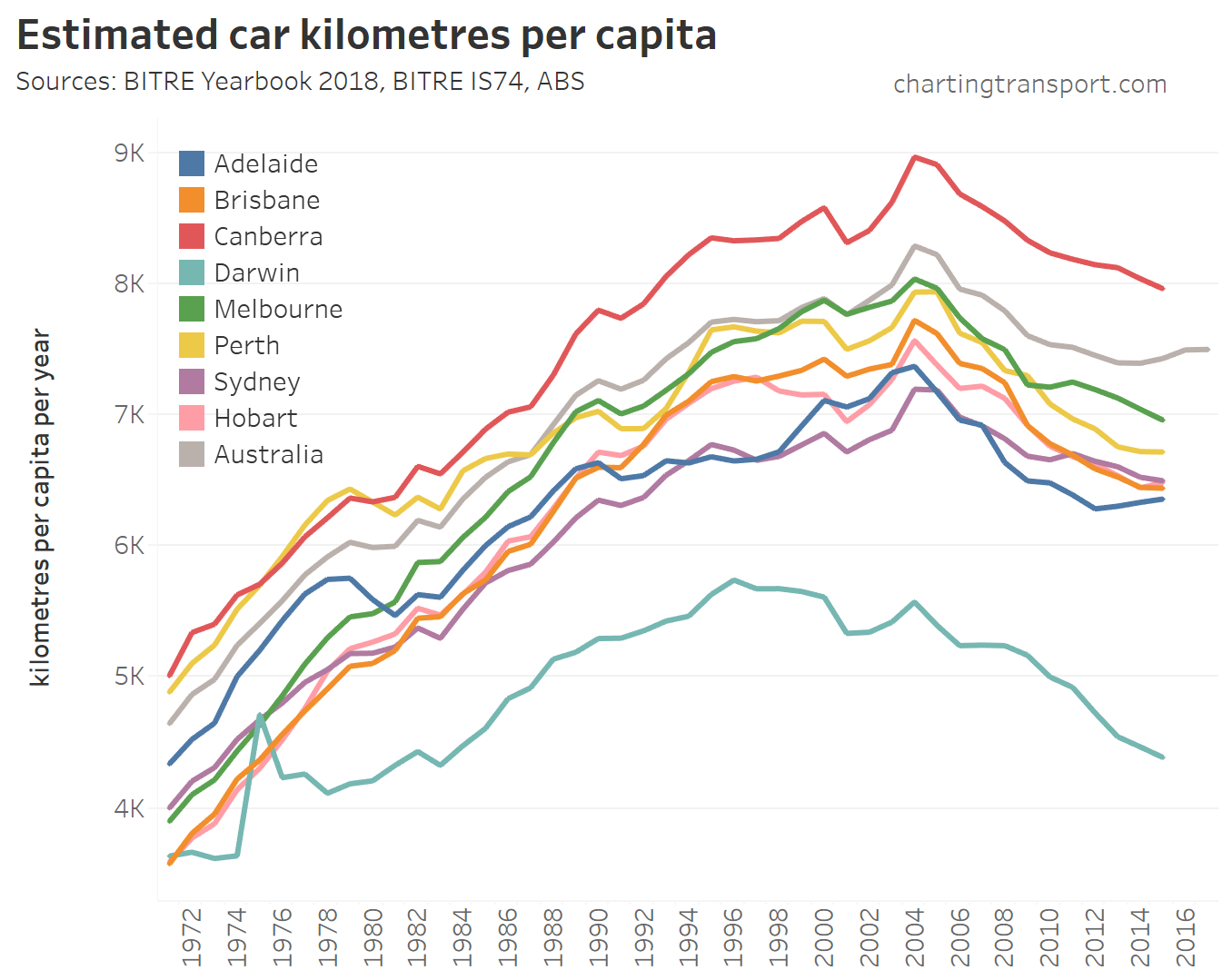

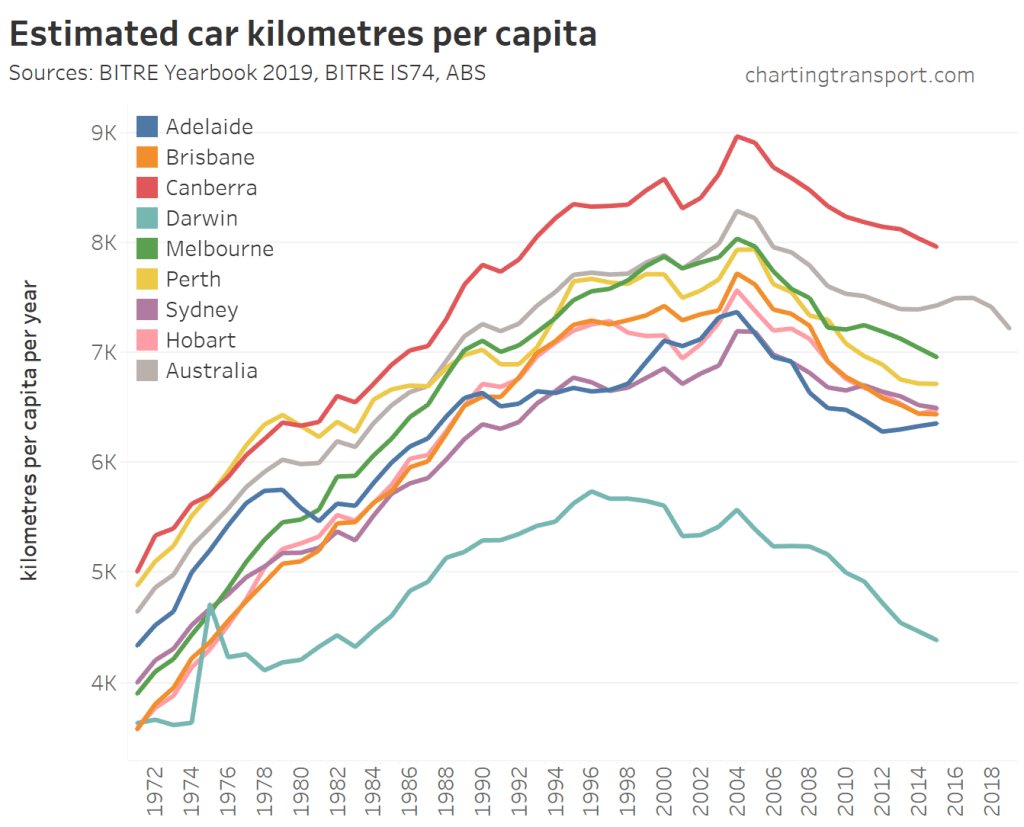

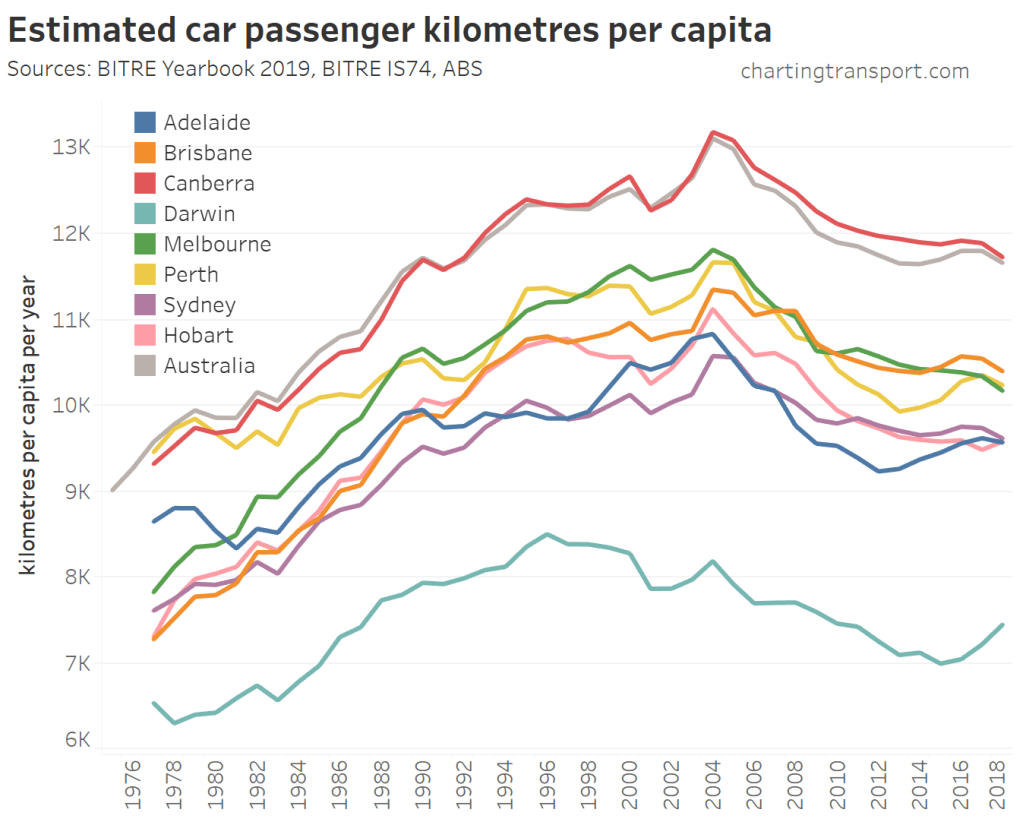

On a per capita basis car use peaked in 2004, with a general decline since then. Here’s the Australian trend (in grey) as well as city level estimates to 2015 (from BITRE Information Sheet 74):

Technical note: “Australia” lines in these charts represent data points for the entire country (including areas outside capital cities).

Darwin has the lowest average which might reflect the small size of the city. The blip in 1975 is related to a significant population exodus after Cyclone Tracey caused significant destruction in late 1974 (the vehicle km estimate might be on the high side).

Canberra, the most car dependent capital city, has had the highest average car kilometres per person (but it might also reflect kilometres driven by people from across the NSW border in Queanbeyan).

The Australia-wide average is higher than most cities, with areas outside capital cities probably involving longer average car journeys and certainly a higher car mode share.

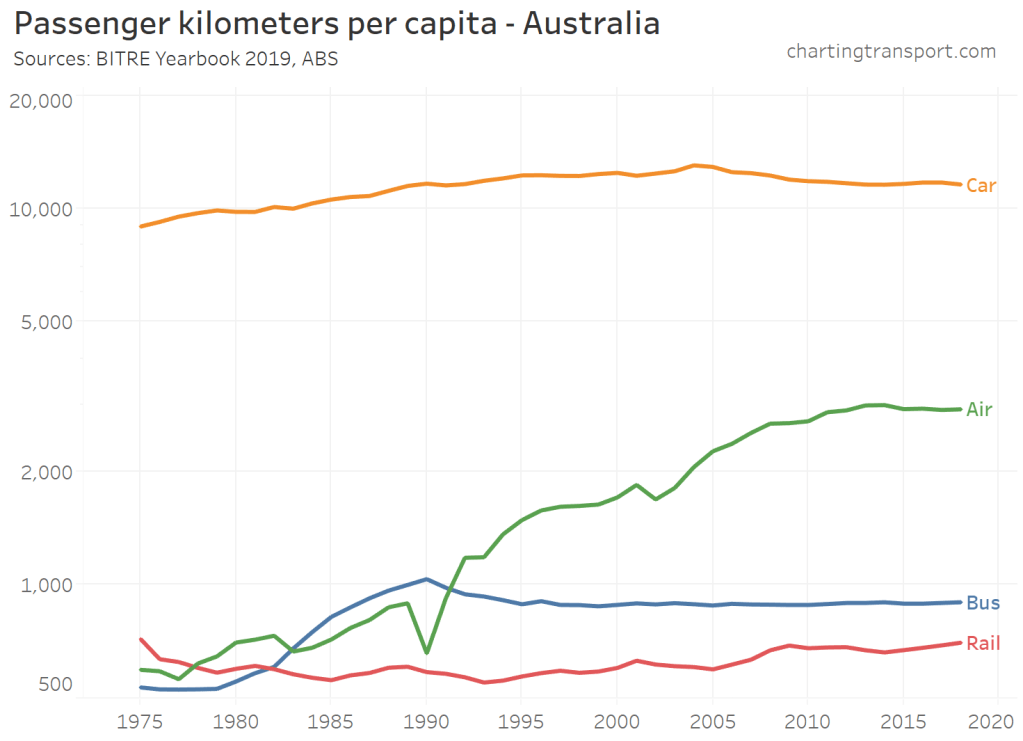

Passenger kilometres travelled

Overall, here are passenger kms per capital for various modes for Australia as a whole (note the log-scale on the Y axis):

Air travel took off (pardon the pun) in the late 1980s (with a lull in 1990), car travel peaked in 2004, bus travel peaked in 1990 and has been relatively flat since, while rail has been increasing in recent years.

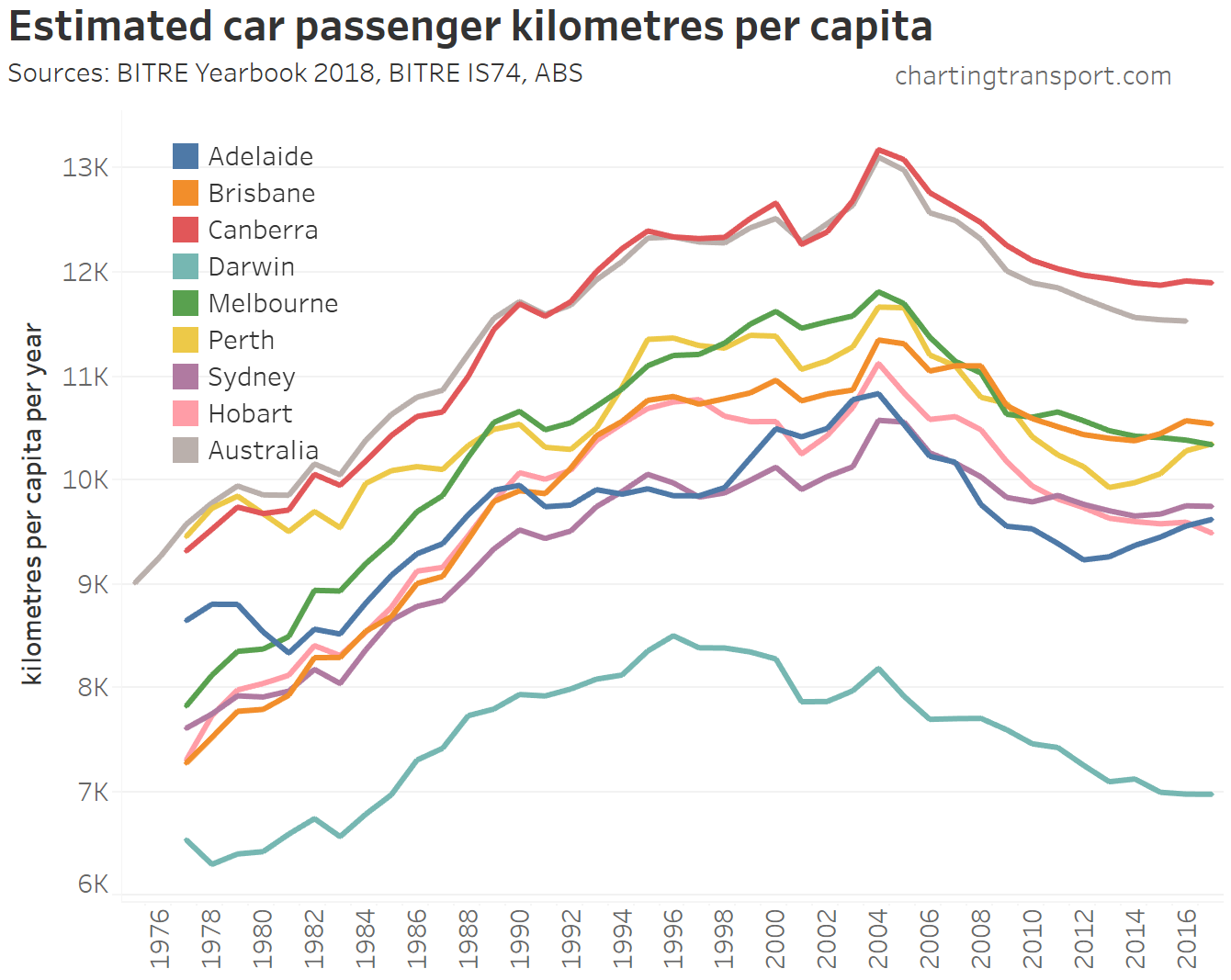

It’s possible to look at car passenger kilometres per capita, which takes into account car occupancy – and also includes more recent estimates up until 2018/19.

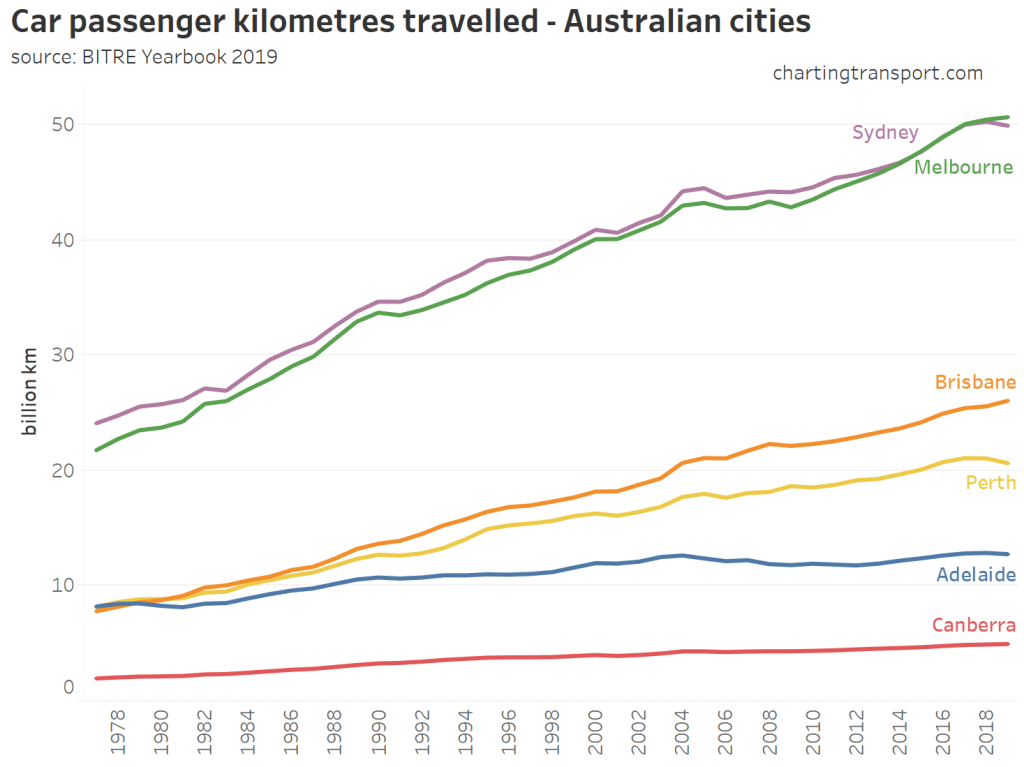

Here’s a chart showing total car passenger kms in each city:

The data shows that Melbourne has now overtaken Sydney as having the most car travel in total.

Another interesting observation is that total car travel declined in Perth, Adelaide, and Sydney in 2018-19. The Sydney result may reflect a mode shift to public transport (more on that shortly), while Perth might be impacted by economic downturn.

While car passenger kilometres per capita peaked in 2004, there were some increases until 2018 in some cities, but most cities declined in 2019. Darwin is looking like an outlier with an increase between 2015 and 2018.

BITRE also produce estimates of passenger kilometres for other modes (data available up to 2017-18 at the time of writing).

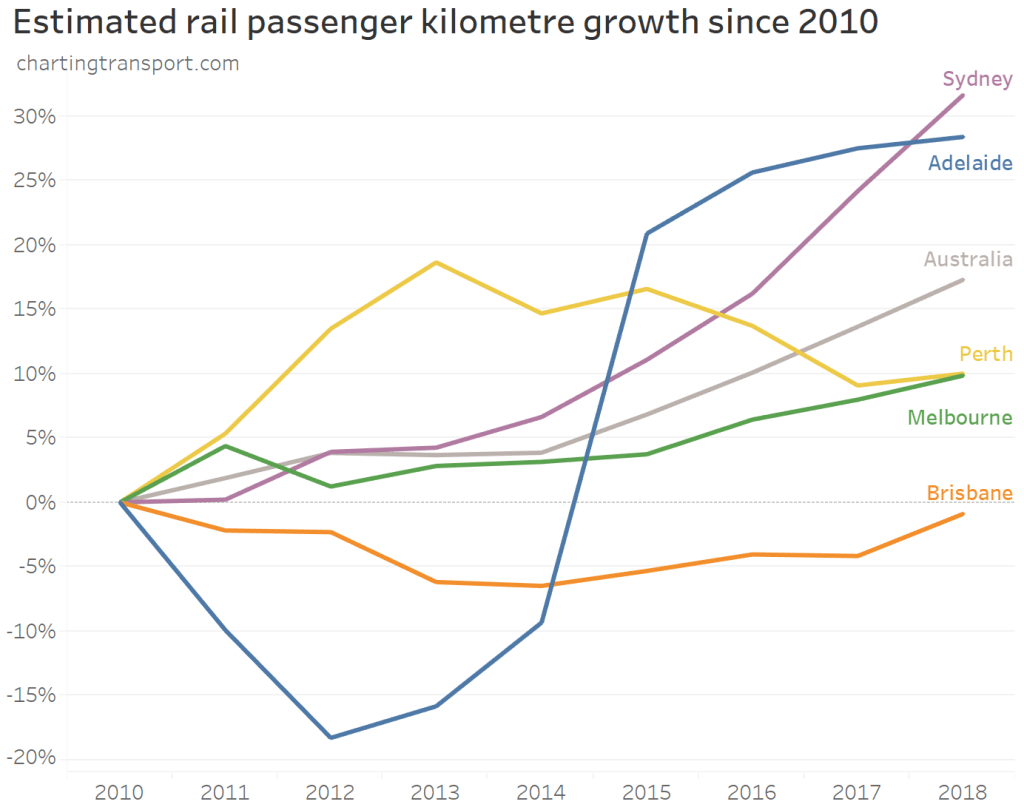

Back to cities, here is growth in rail passenger kms since 2010:

Sydney trains have seen rapid growth in the last few years, probably reflecting significant service level upgrades to provide more stations with “turn up and go” frequencies at more times of the week.

Adelaide’s rail patronage dipped in 2012, but then rebounded following completion of the first round of electrification in 2014.

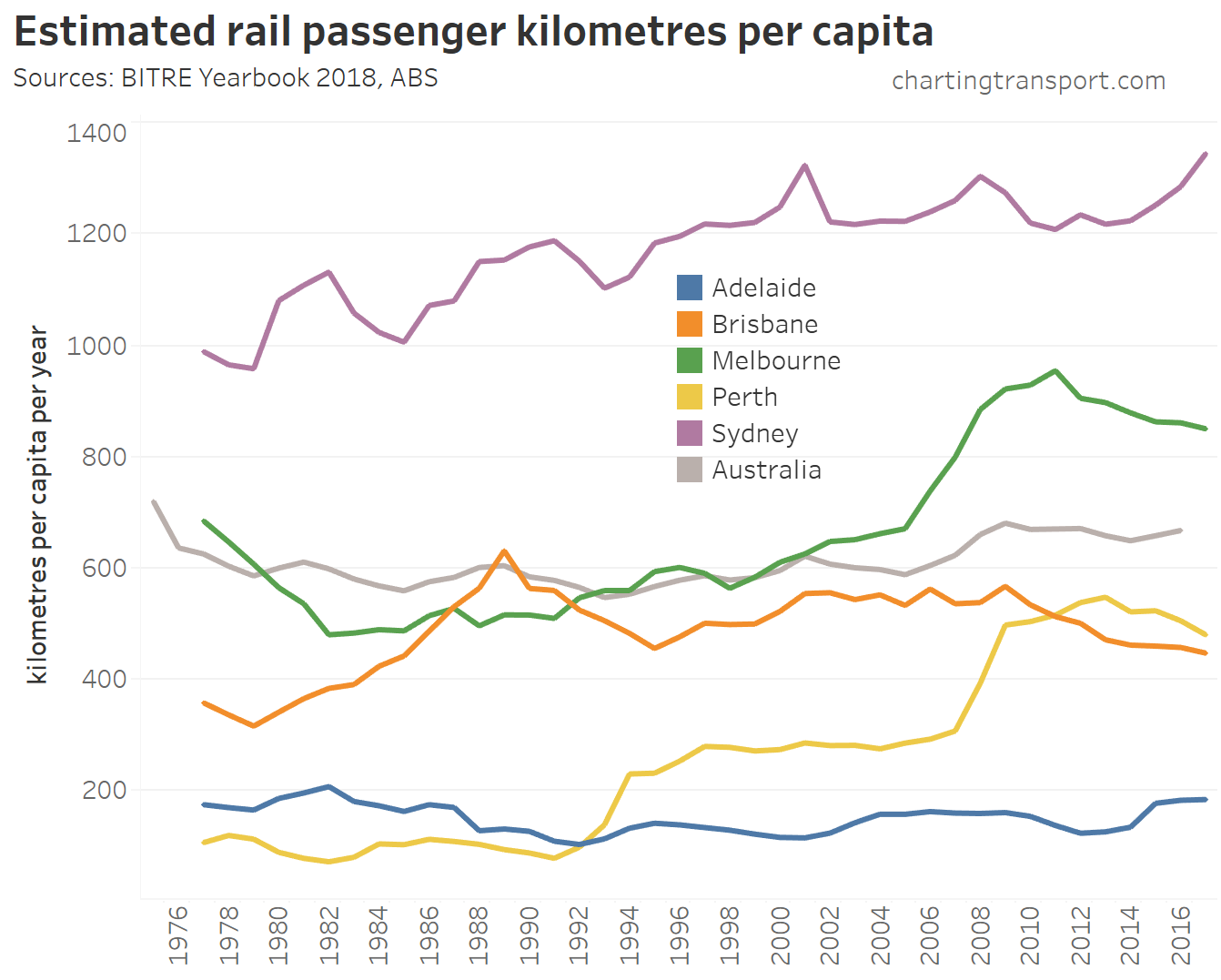

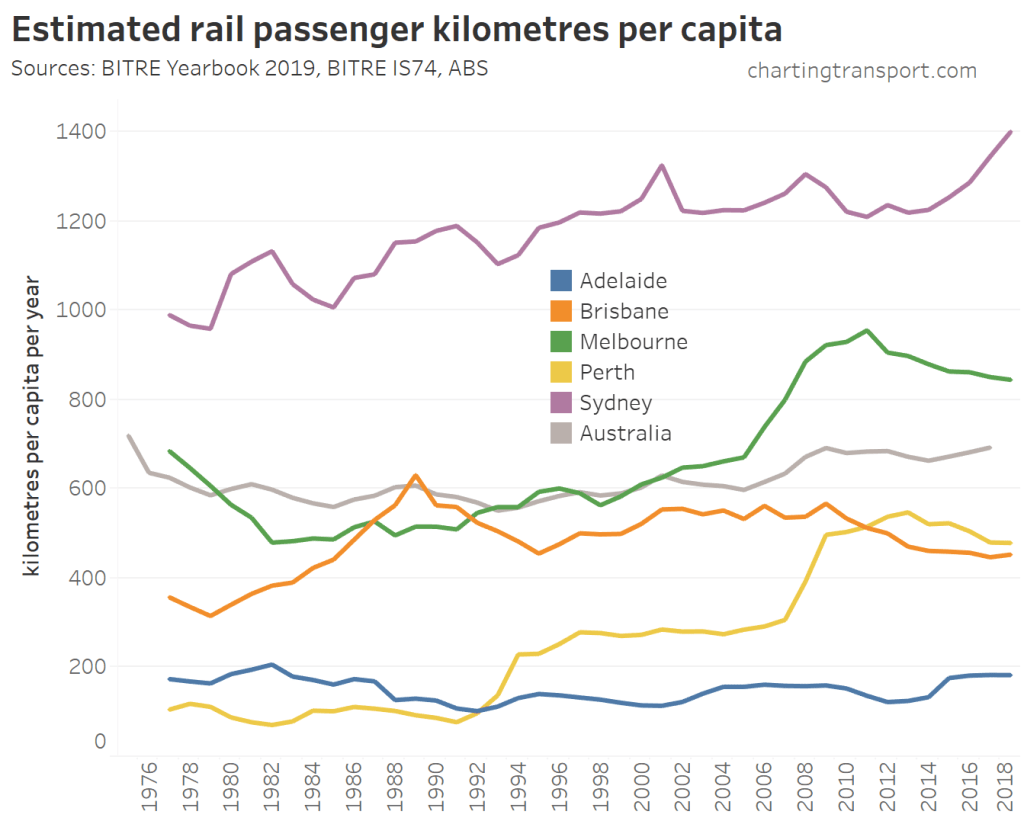

Here’s a longer-term series looking at per-capita train use:

Sydney has the highest train use of all cities. You can see two big jumps in Perth following the opening of the Joondalup line in 1992 and the Mandurah line in 2007. Melbourne, Brisbane and Perth have shown declines over recent years.

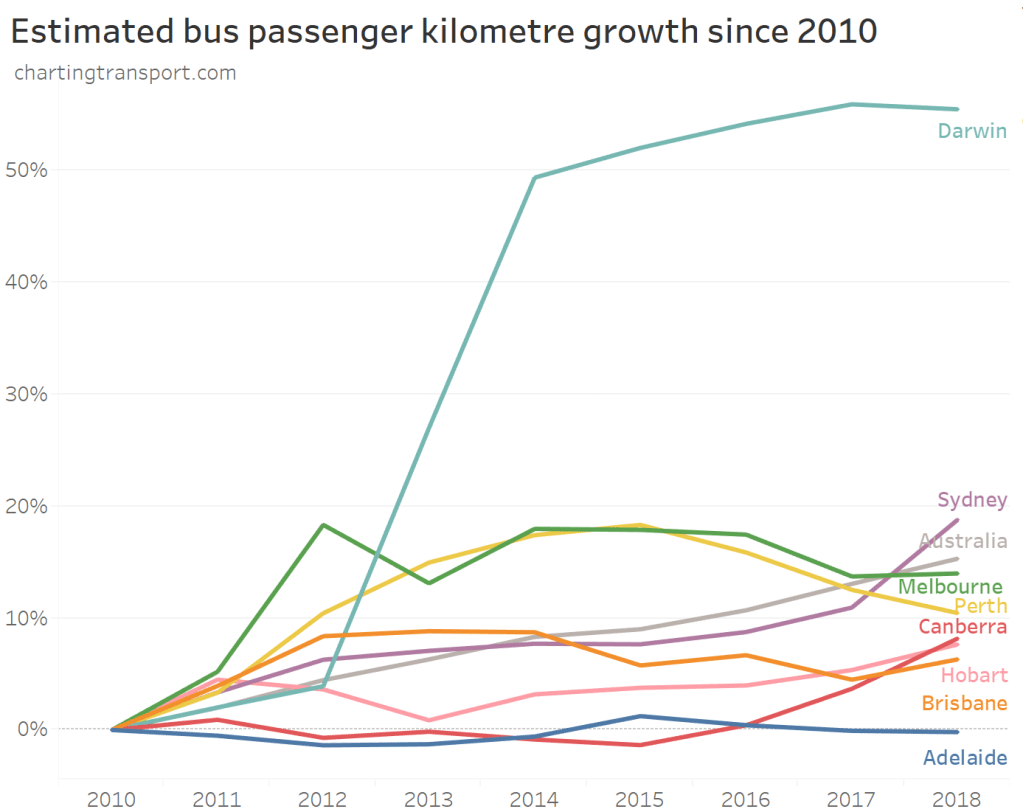

Here is recent growth in (public and private) bus use:

Darwin saw a massive increase in bus use in 2014 thanks to a new nearby LNG project running staff services.

In more recent years Sydney, Canberra, and Hobart are showing rapid growth in bus patronage.

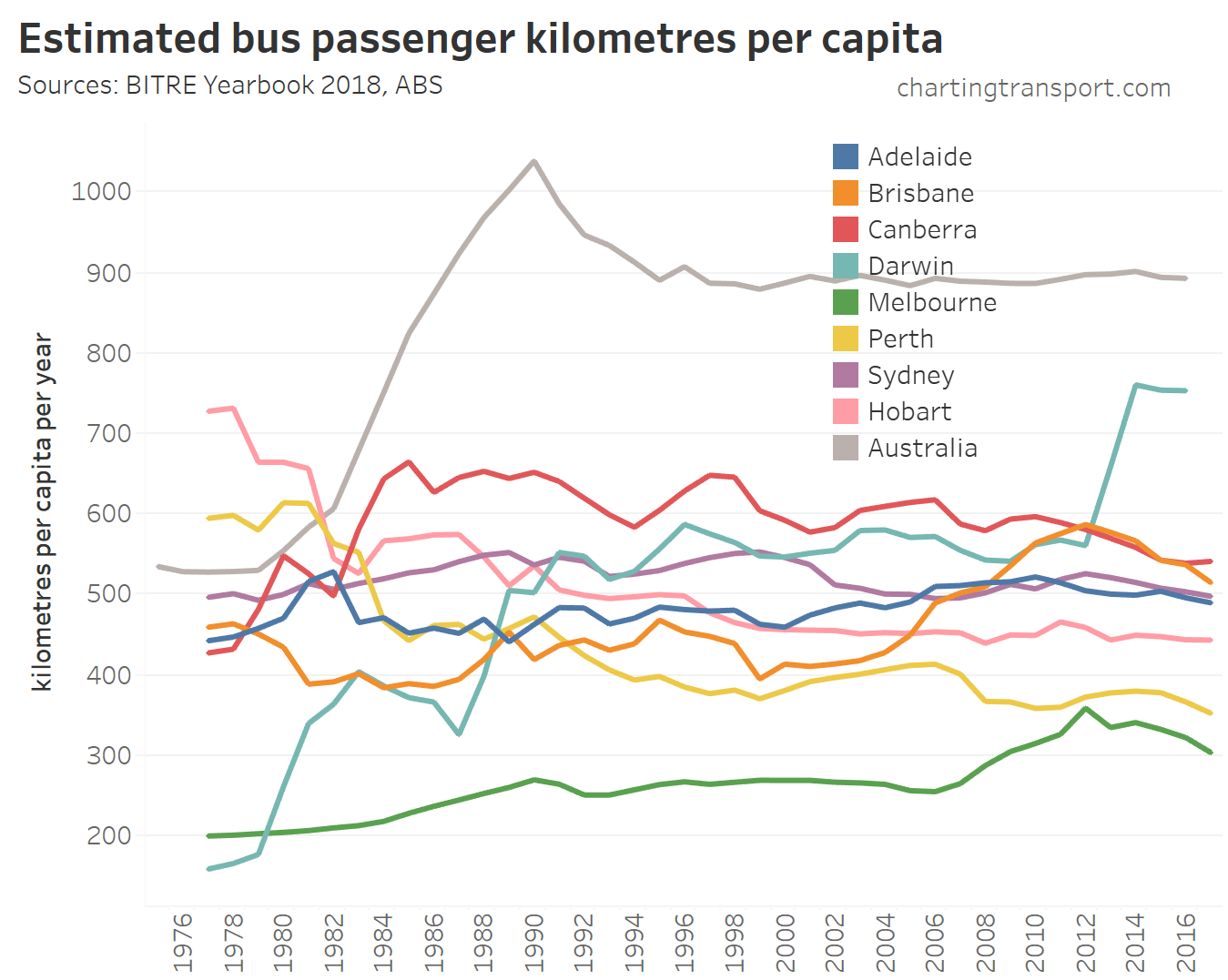

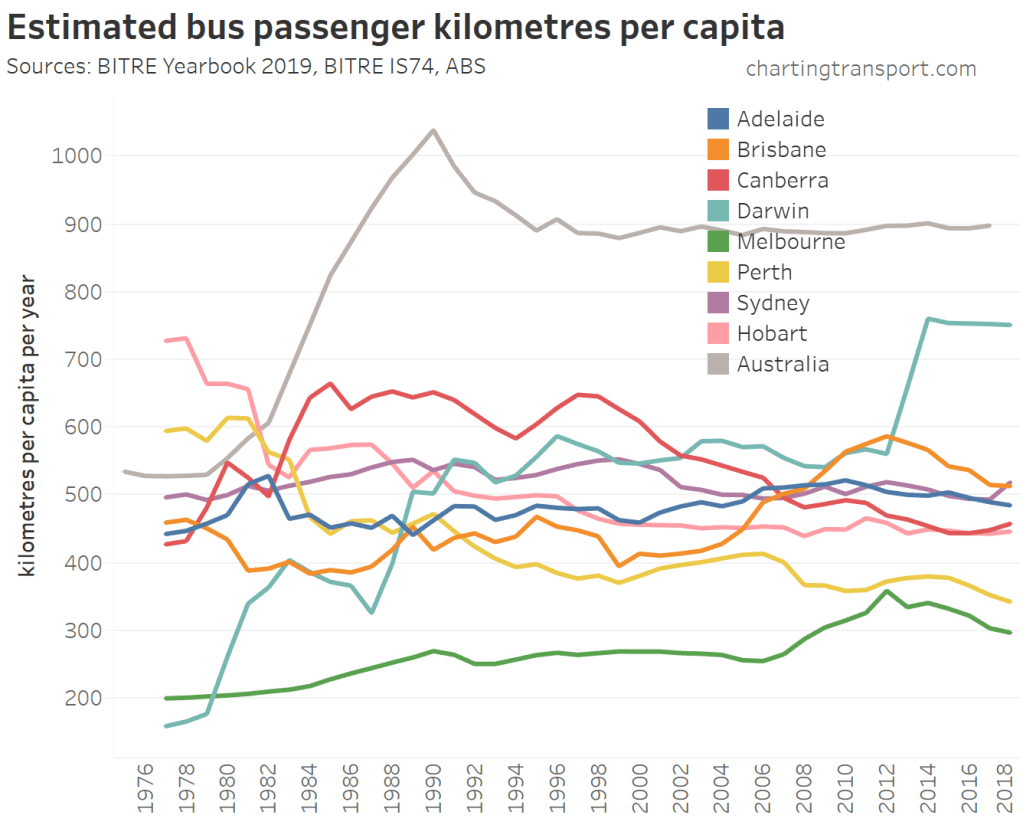

Here’s bus passenger kms per capita:

Investments in increased bus services in Melbourne and Brisbane between around 2005 and 2012 led to significant patronage growth.

Bus passenger kms per capita have been declining in most cities in recent years.

Australia-wide bus usage is surprisingly high. While public transport bus service levels and patronage would certainly be on average low outside capital cities, buses do play a large role in carrying children to school – particularly over longer distances in rural areas. The peak for bus usage in 1990 may be related to deregulation of domestic aviation, which reduced air fares by around 20%.

Melbourne has the lowest bus use of all the cities, but this likely reflects the extensive train and tram networks carrying the bulk of the public transport passenger task. Melbourne is different to every other Australian city in that trams provide most of the on-road public transport access to the CBD (with buses performing most of this function in other cities).

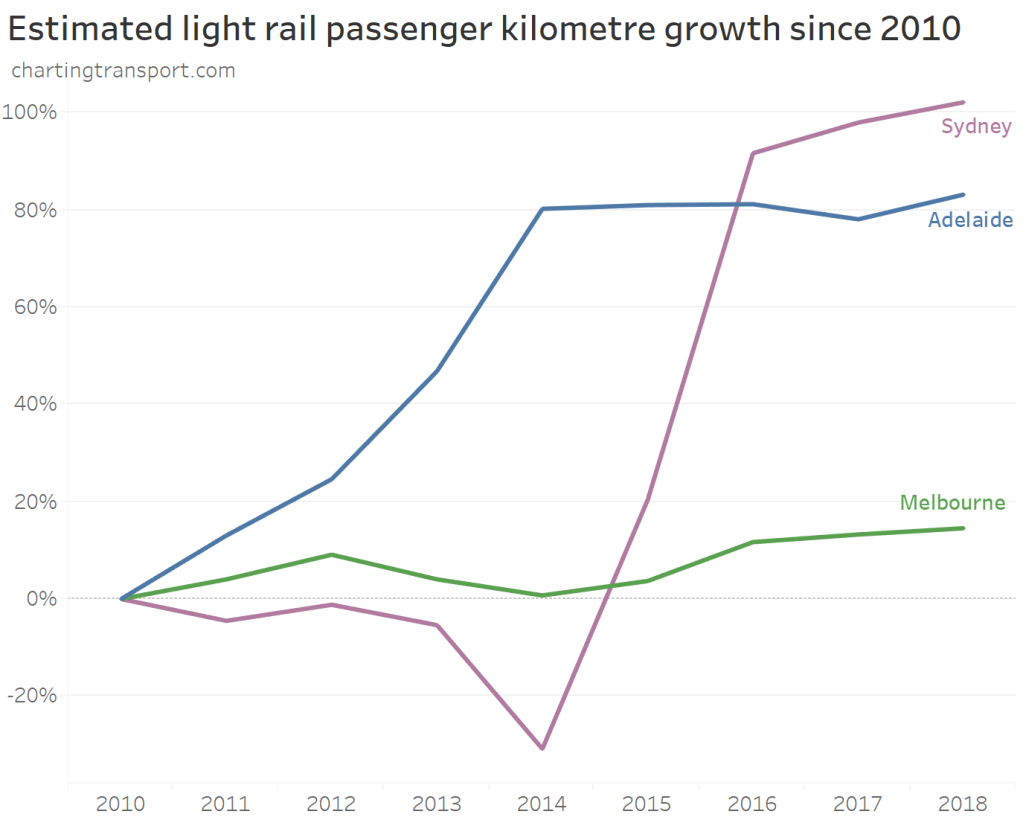

For completeness, here’s growth in light rail patronage:

Sydney light rail patronage increased following the Dulwich Hill extension that opened in 2014, while Adelaide patronage increased following an extension to the Adelaide Entertainment Centre in 2010.

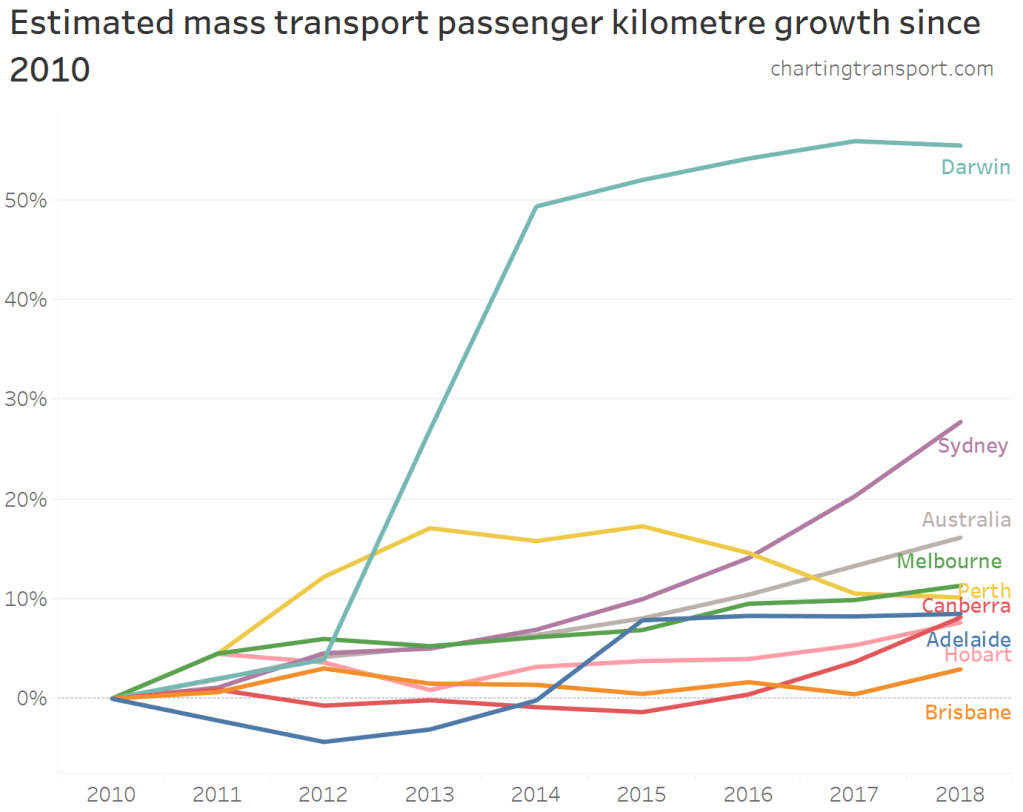

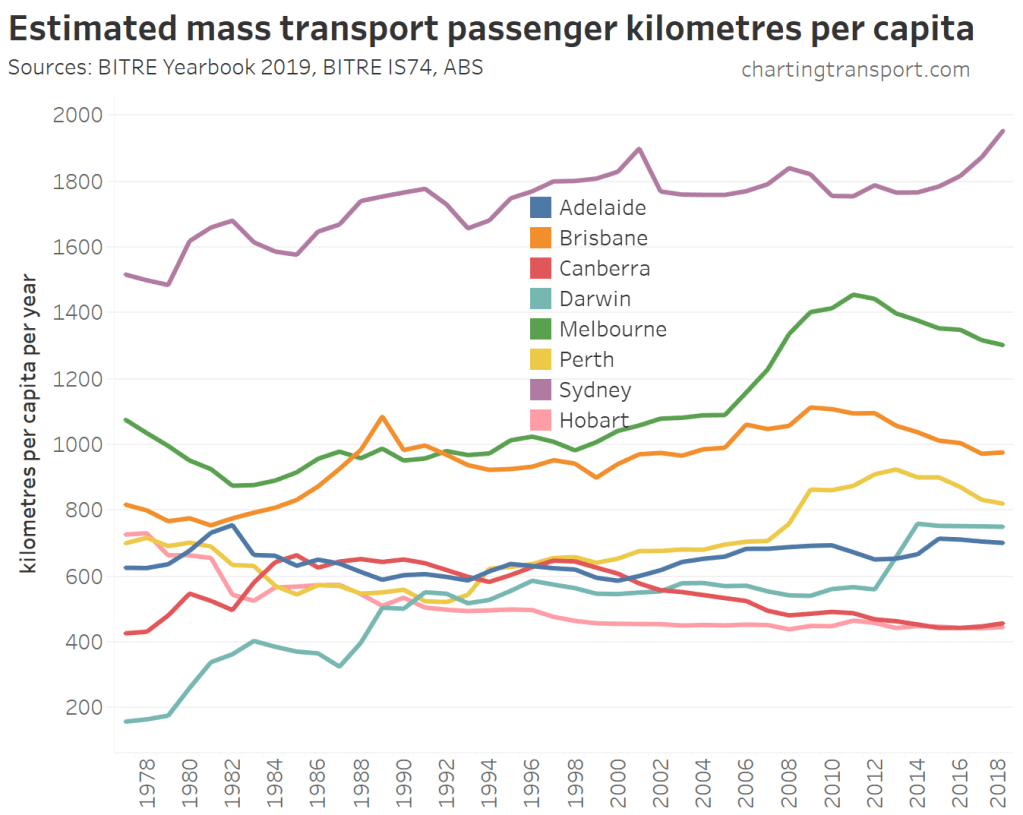

We can sum all of the mass transit modes (I use the term “mass transit” to account for both public and private bus services):

Sydney is leading the country in mass transport use per capita and is growing strongly, while Melbourne, Brisbane, Perth have declined in recent years.

Mass transit mode share

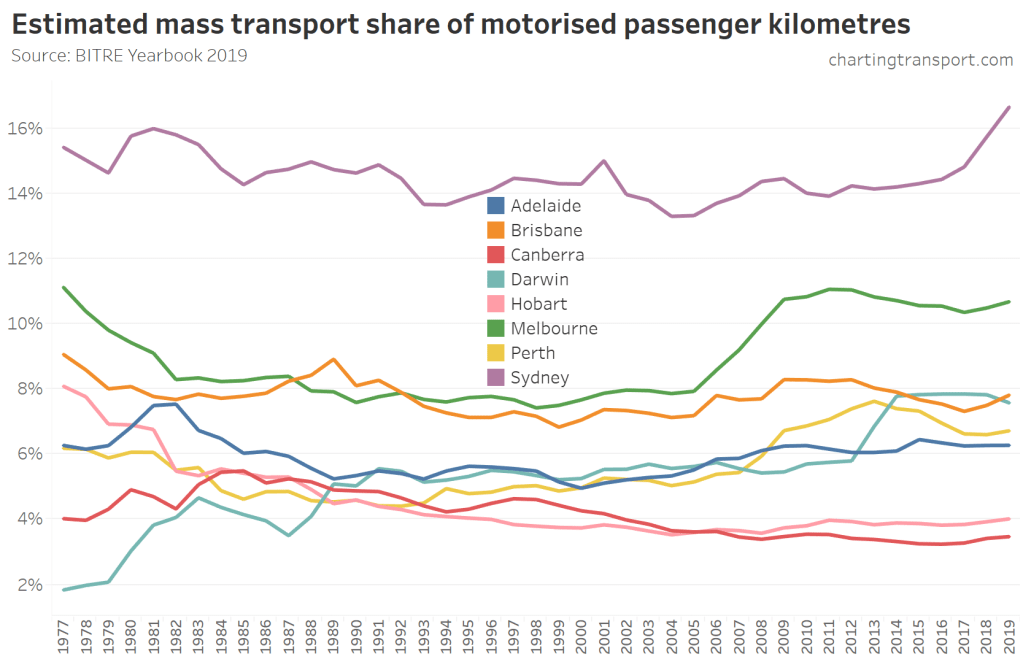

We can also calculate mass transit mode share of motorised passenger kilometres (walking and cycling kilometres are unfortunately not estimated by BITRE):

Sydney has maintained the highest mass transit mode share, and in recent years has grown rapidly with a 3% mode shift in the three years 2016 to 2019, mostly attributable to trains. The Sydney north west Metro line opened in May 2019, so would only have a small impact on these figures.

Melbourne made significant gains between 2005 and 2009, and Perth also grew strongly 2007 to 2013.

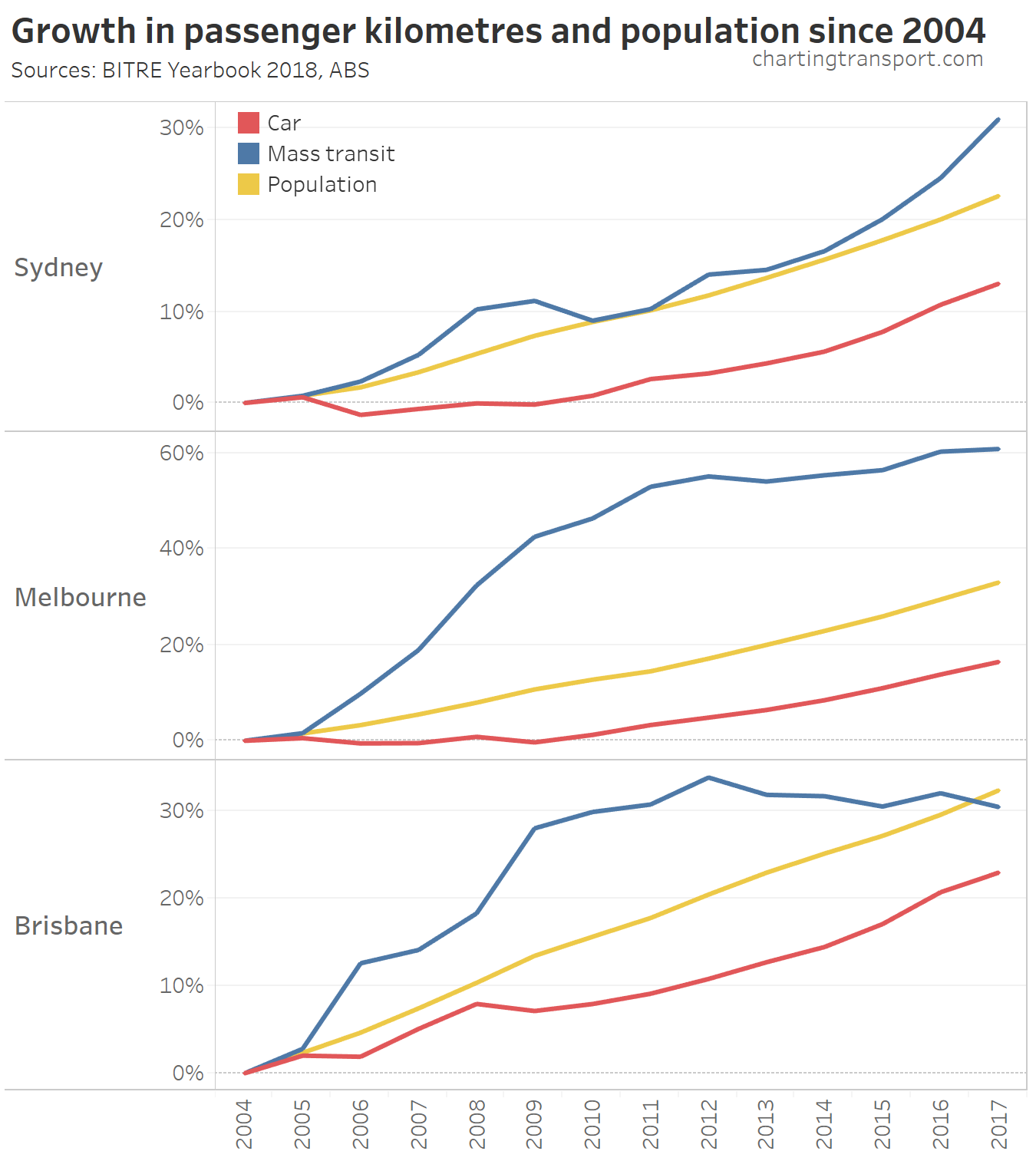

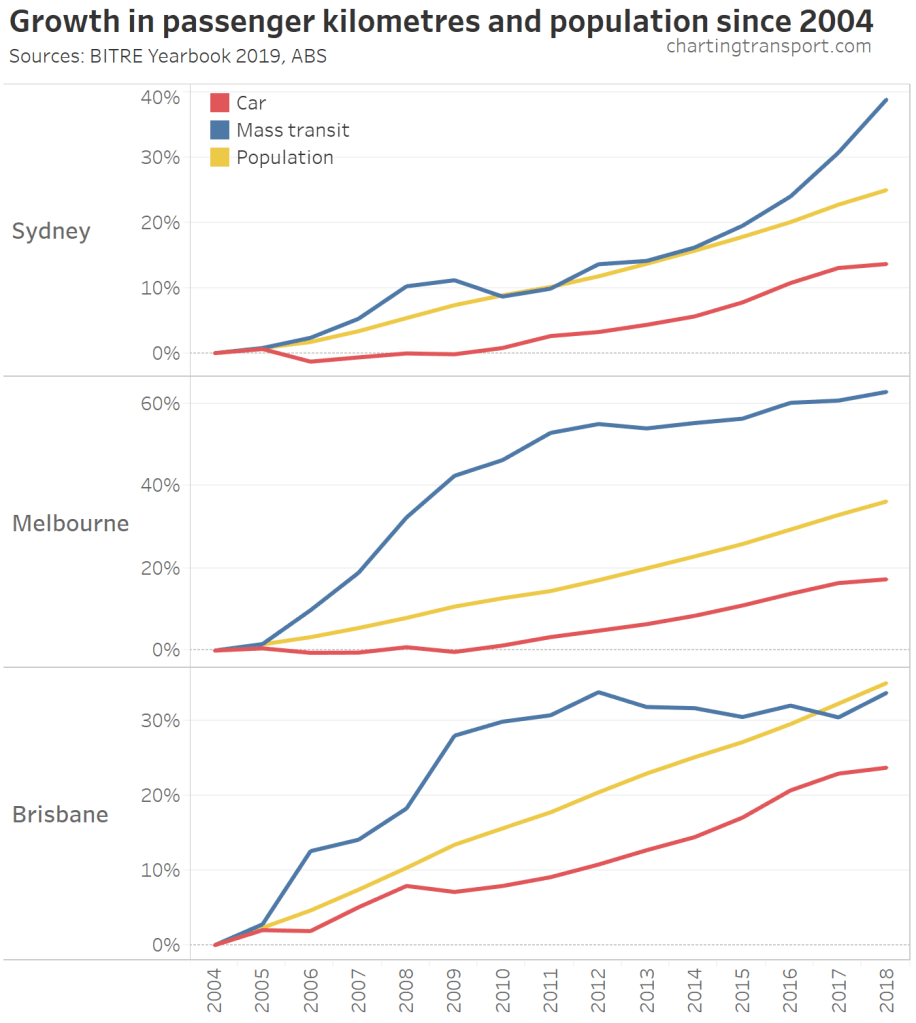

Here’s how car and mass transit passenger kilometres have grown since car used peaked in 2004:

Mass transit use has grown much faster than car use in Australia’s three largest cities. In Sydney and Melbourne it has exceeded population growth, while in Brisbane it is more recently tracking with population growth.

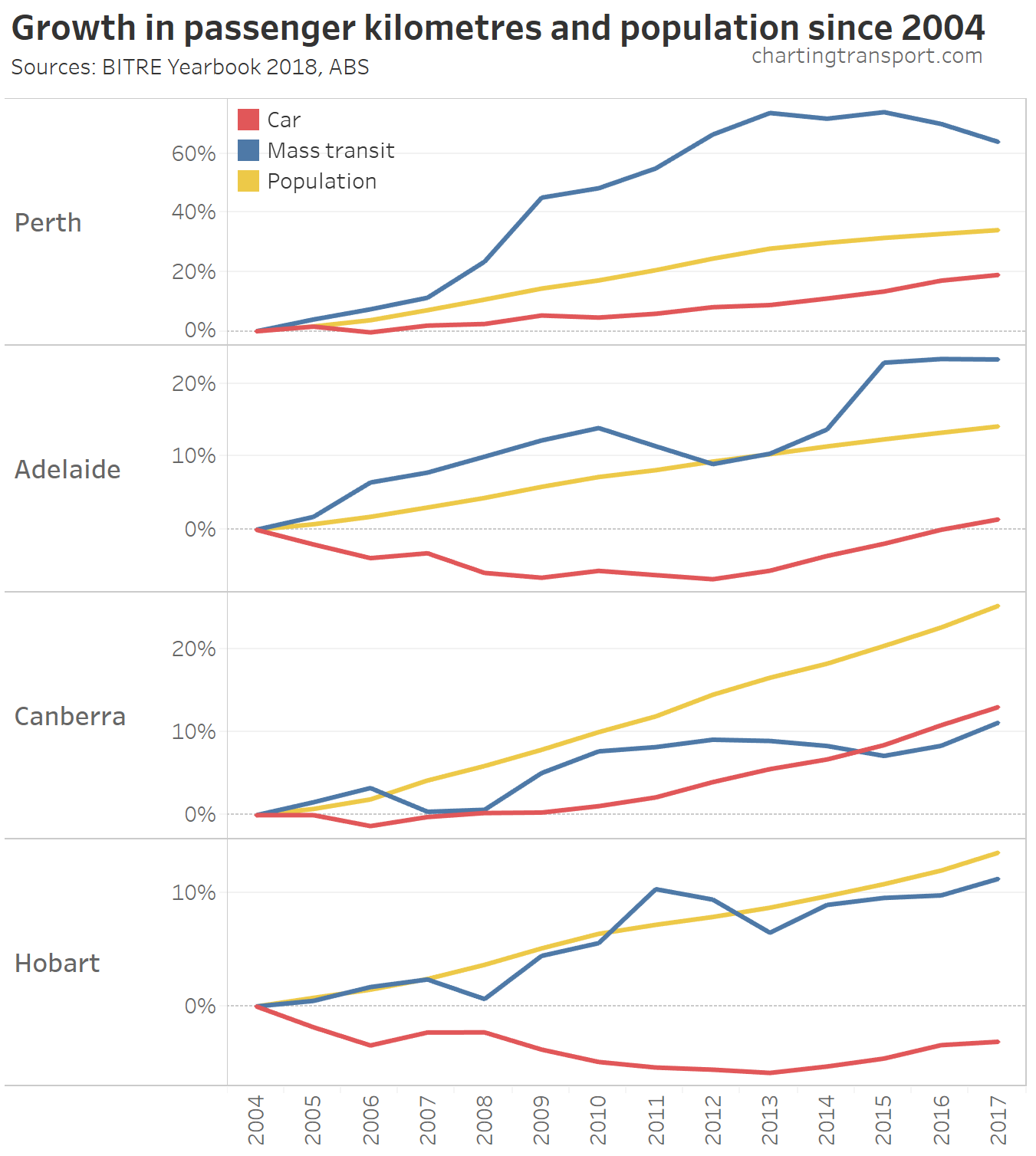

Mass transit has also outpaced car use in Perth, Adelaide, and Hobart:

In Canberra, both car and mass transit use has grown much slower than population, and it is the only city where car growth has exceeded public transport growth.

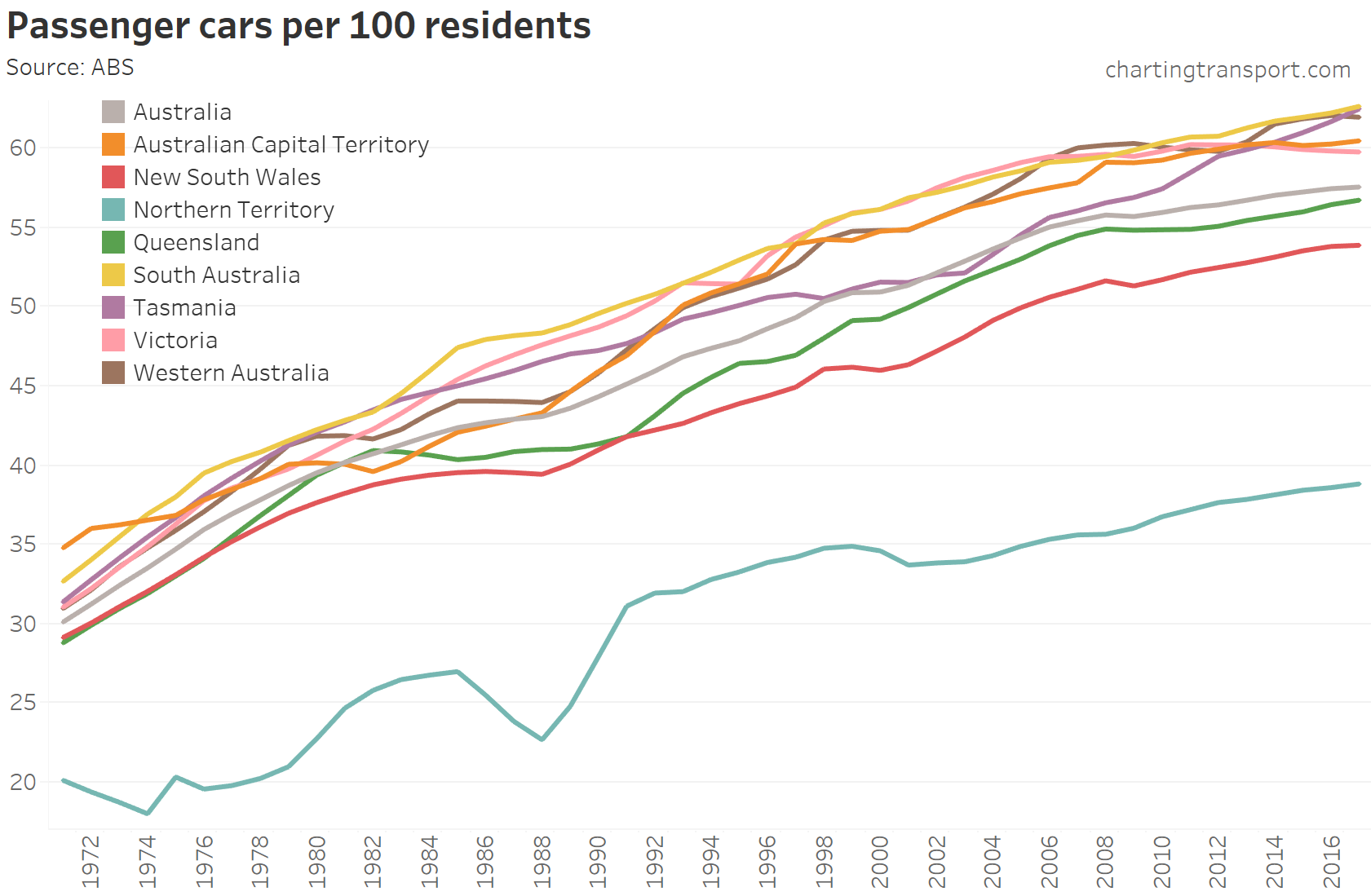

Car ownership

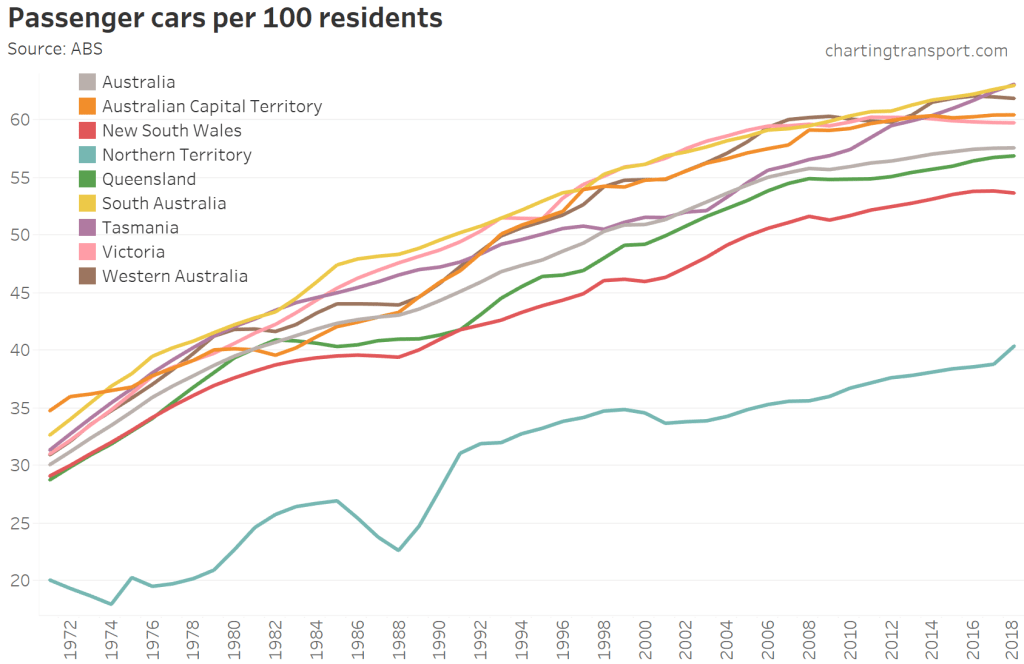

The ABS regularly conduct a Motor Vehicle Census, and the following chart includes data up until January 2019.

Technical note: Motor Vehicle Census data (currently conducted in January each year, but previously conducted in March or October) has been interpolated to produce June estimates for each year, with the latest estimate being for June 2018.

In 2017-18 car ownership declined slightly in New South Wales, Victoria, and Western Australia, but there was a significant increase in the Northern Territory. Tasmania has just overtaken South Australia as the state with the highest car ownership at 63.1 cars per 100 residents.

Victorian car ownership has been in decline since 2011, which is consistent with a finding of declining motor vehicle ownership in Melbourne from census data (see also an older post on car ownership).

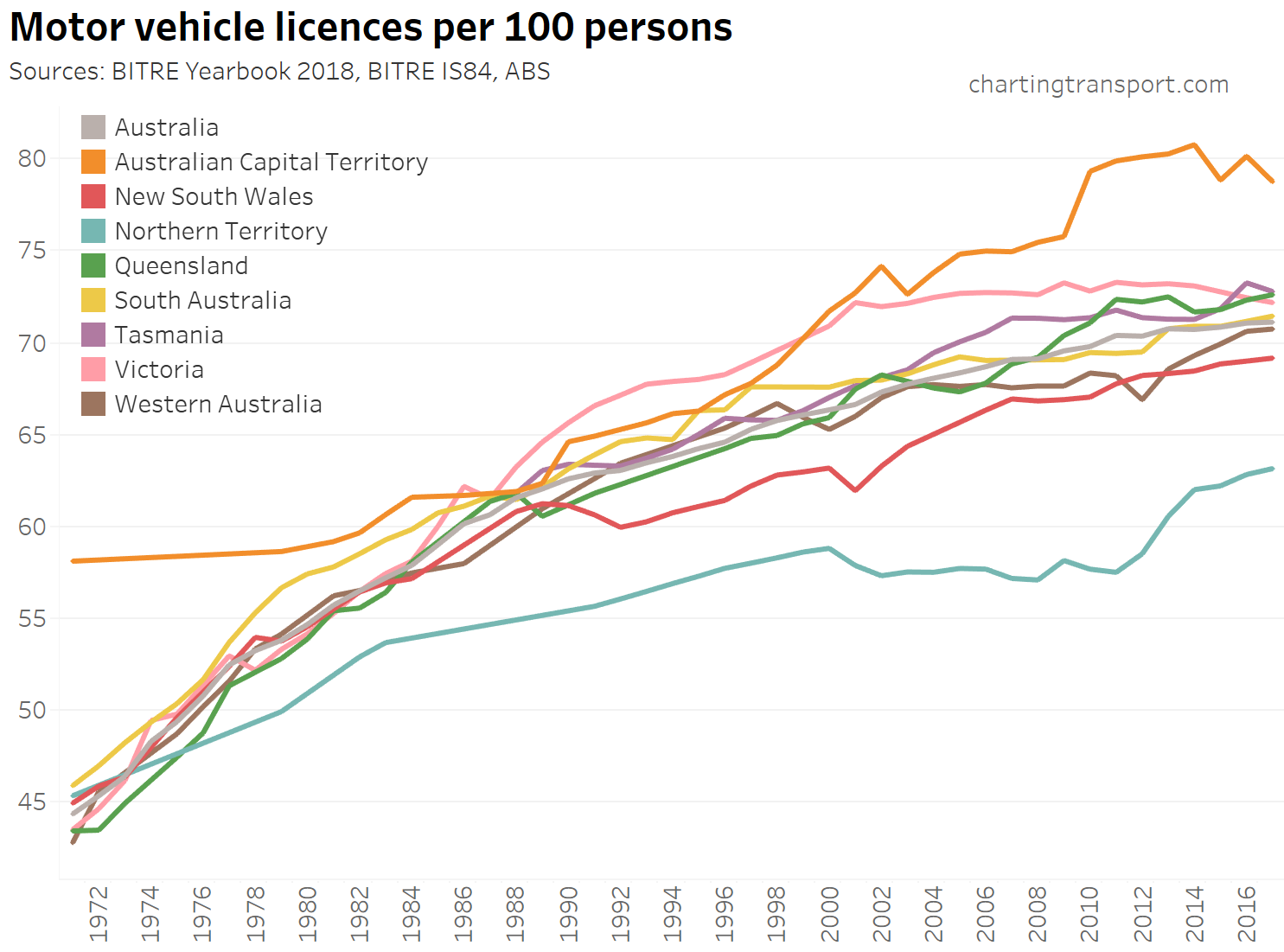

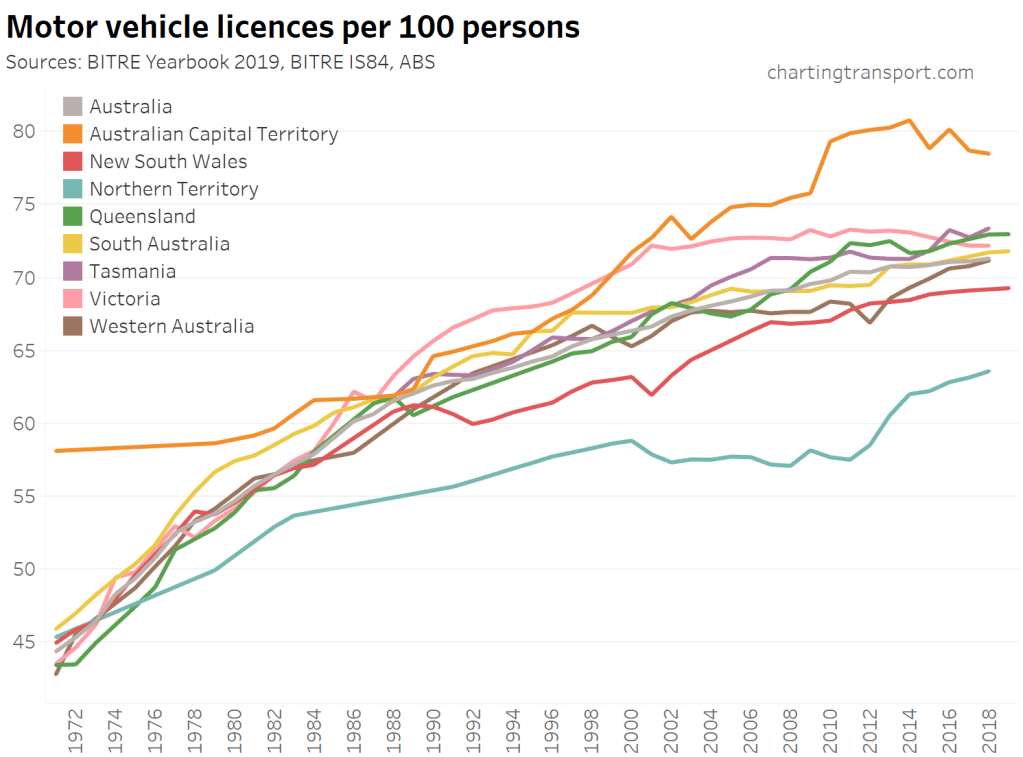

Driver’s licence ownership

Thanks to BITRE Information Sheet 84, the BITRE Yearbook 2019, and some useful state government websites (NSW, SA, Qld), here is motor vehicle licence ownership per 100 persons (of any age) from June 1971 to June 2018 or 2019 (depending on data availability):

Technical note: the ownership rate is calculated as the sum of car, motorbike and truck licenses – including learner and probationary licences, divided by population. Some people have more than one driver’s licence so it’s likely to be an over-estimate of the proportion of the population with any licence.

There’s been slowing growth over time, but Victoria has seen slow decline since 2011, and the ACT peaked in 2014.

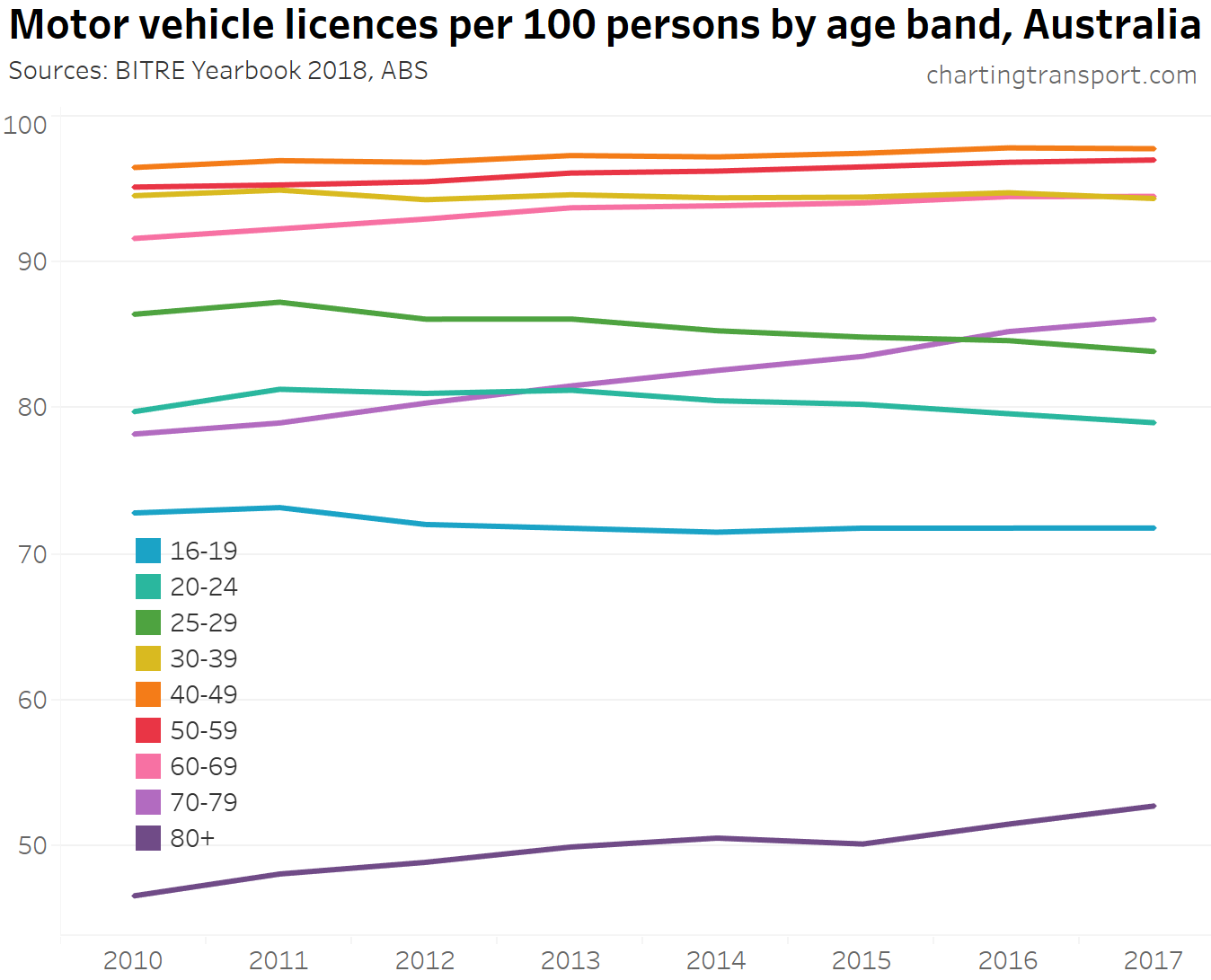

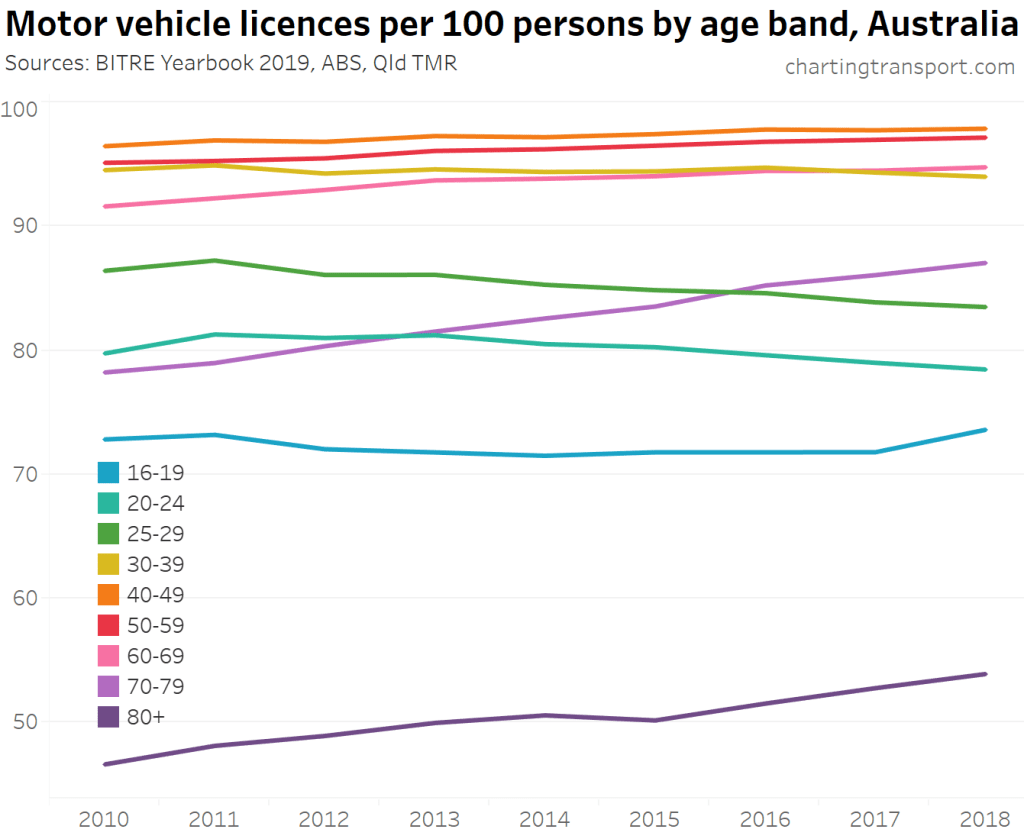

Here’s a breakdown by age bands for Australia as a whole (note each chart has a different Y-axis scale):

There was a notable uptick in licence ownership for 16-19 year-olds in 2018. Otherwise licencing rates have increased for those over 40, and declined for those aged 20-39.

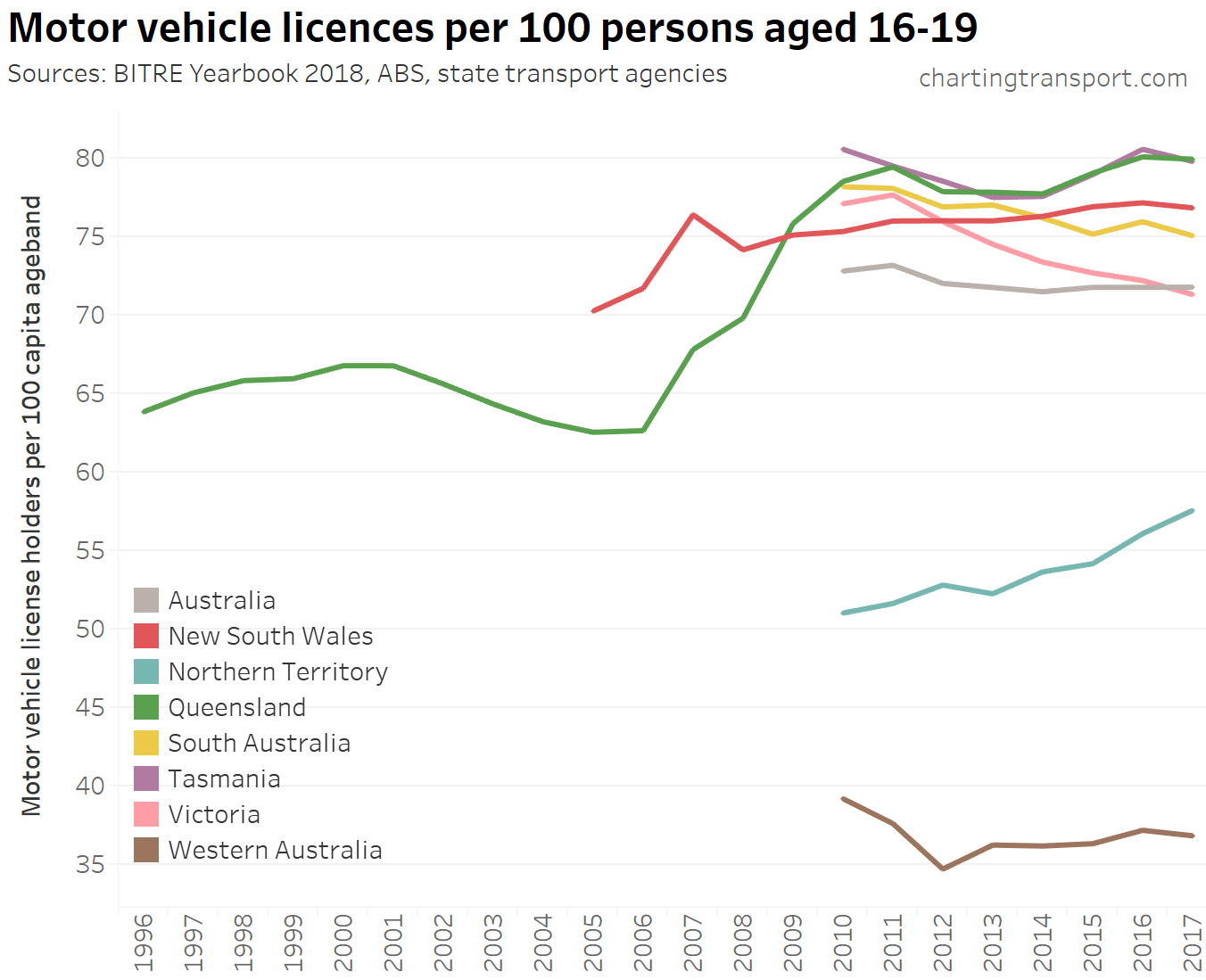

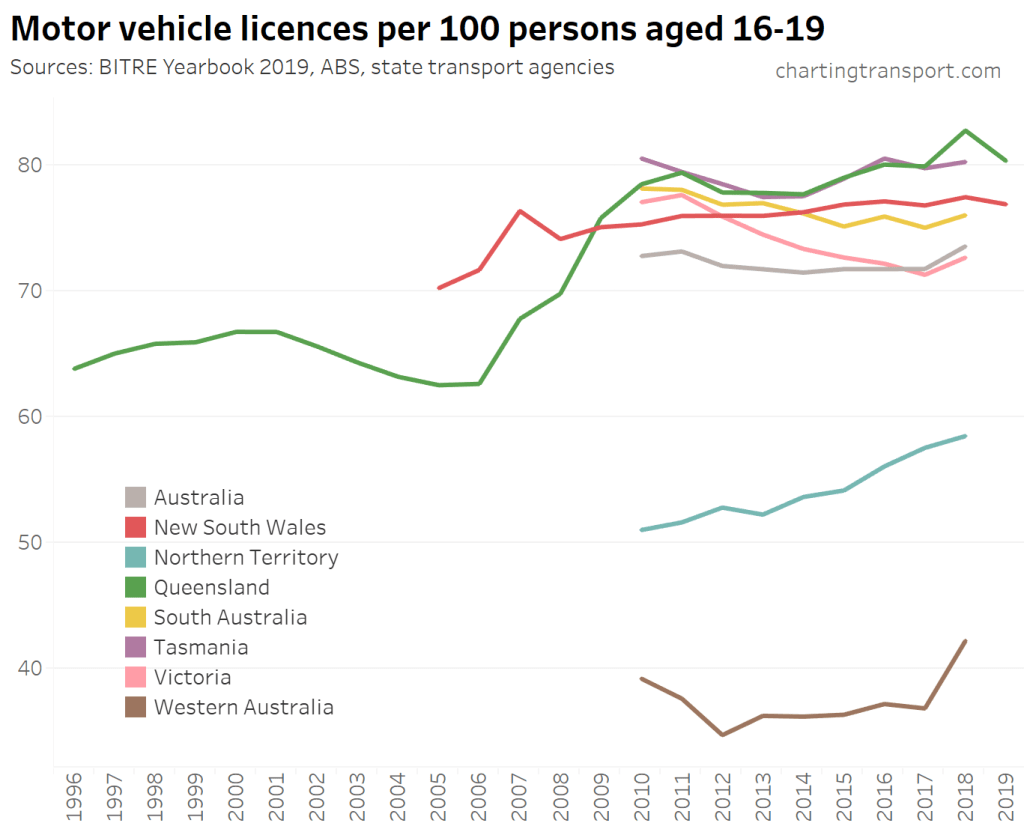

Licencing rates for teenagers (refer next chart) had been trending down in South Australia and Victoria until 2017, but all states saw an increase in 2018 (particularly Western Australia). The most recent 2019 data from NSW and Queensland shows a decline. The differences between states partly reflects different minimum ages for licensing.

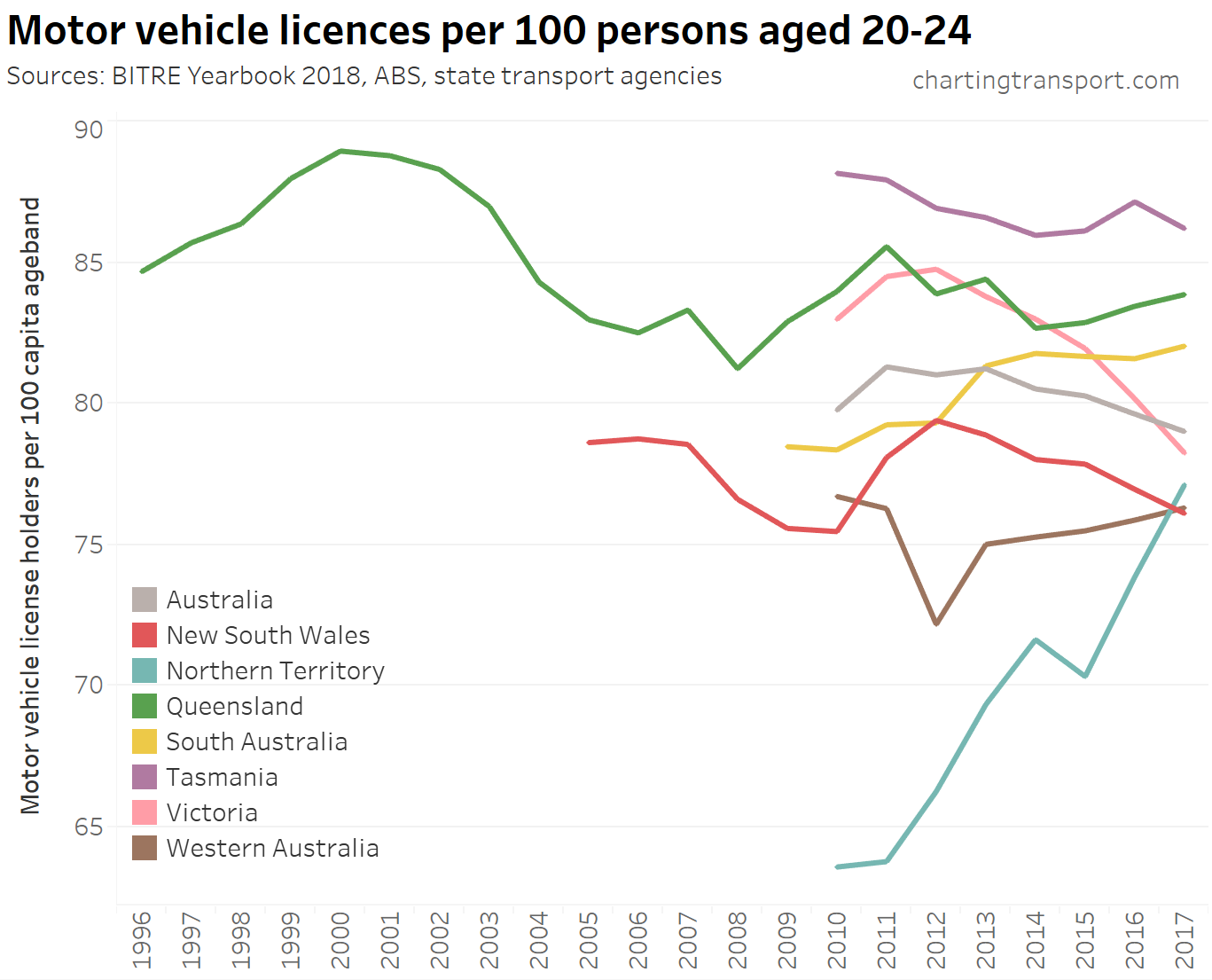

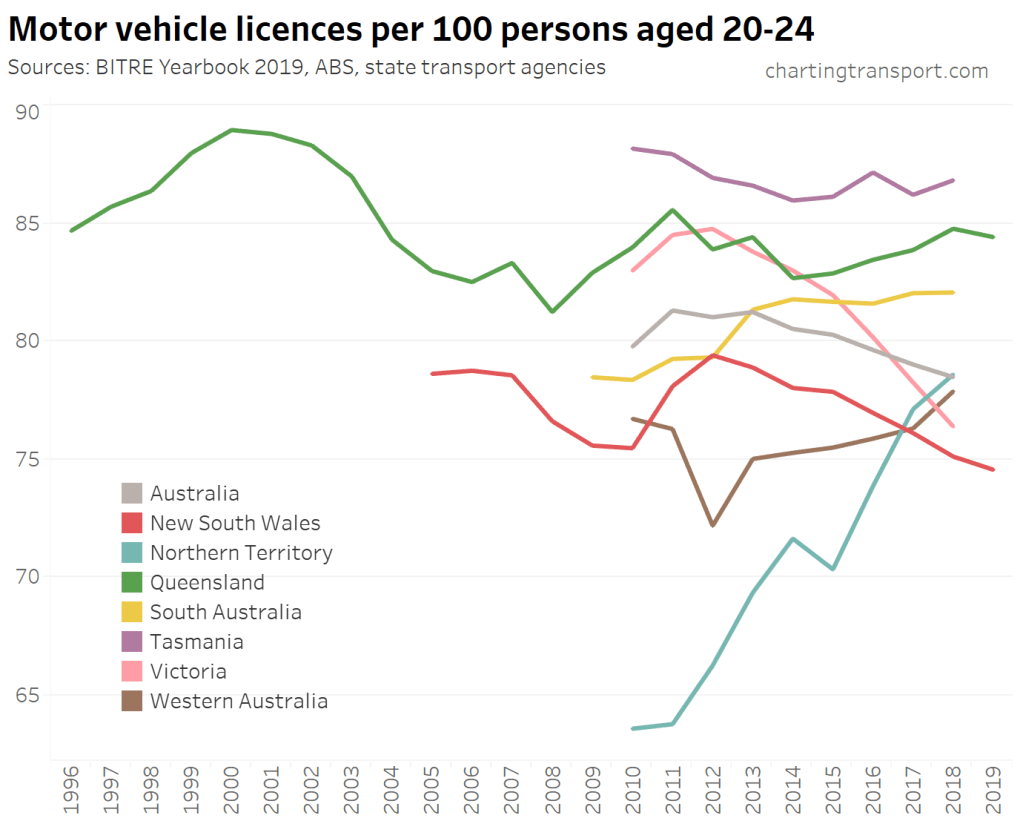

The trends are mixed for 20-24 year-olds: the largest states of Victoria and New South Wales have seen continuing declines in licence ownership, but all other states and territories are up (except Queensland in 2019).

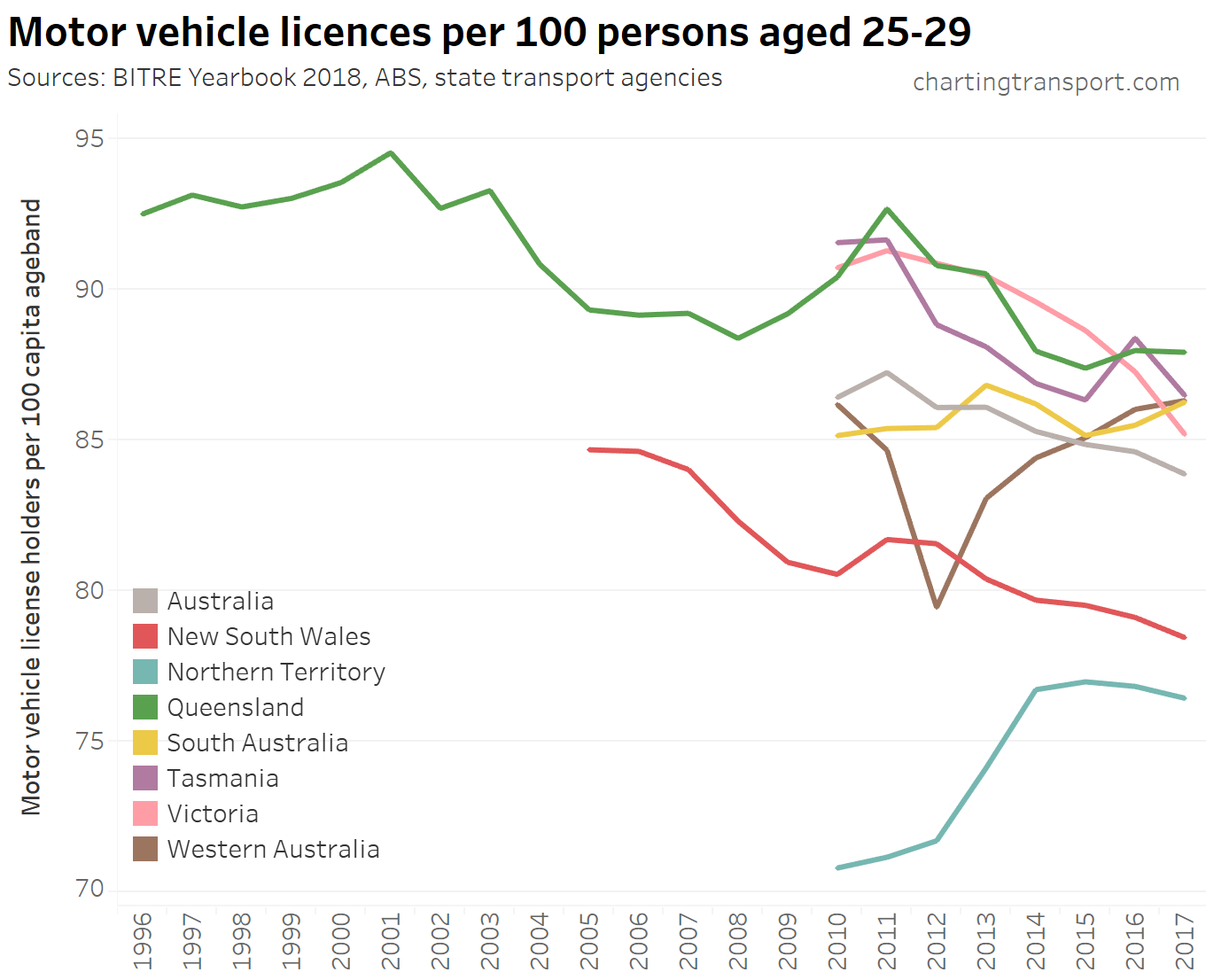

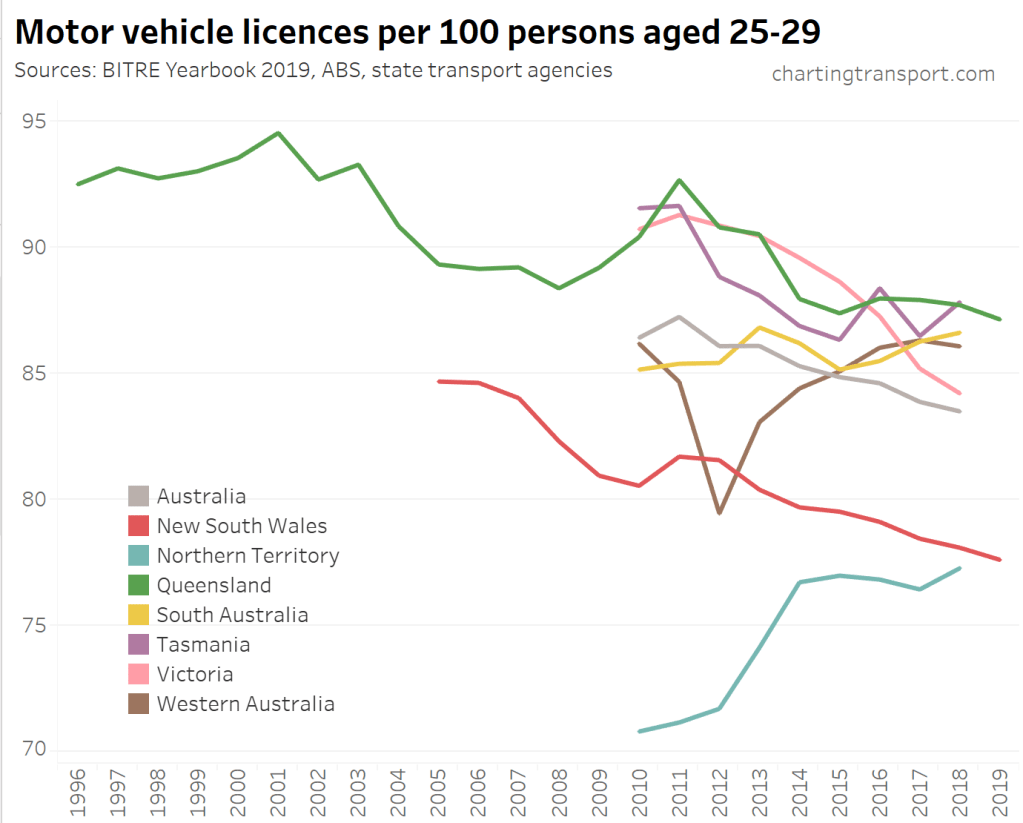

New South Wales, Victoria, and – more recently – Queensland are seeing downward trends in the 25-29 age bracket:

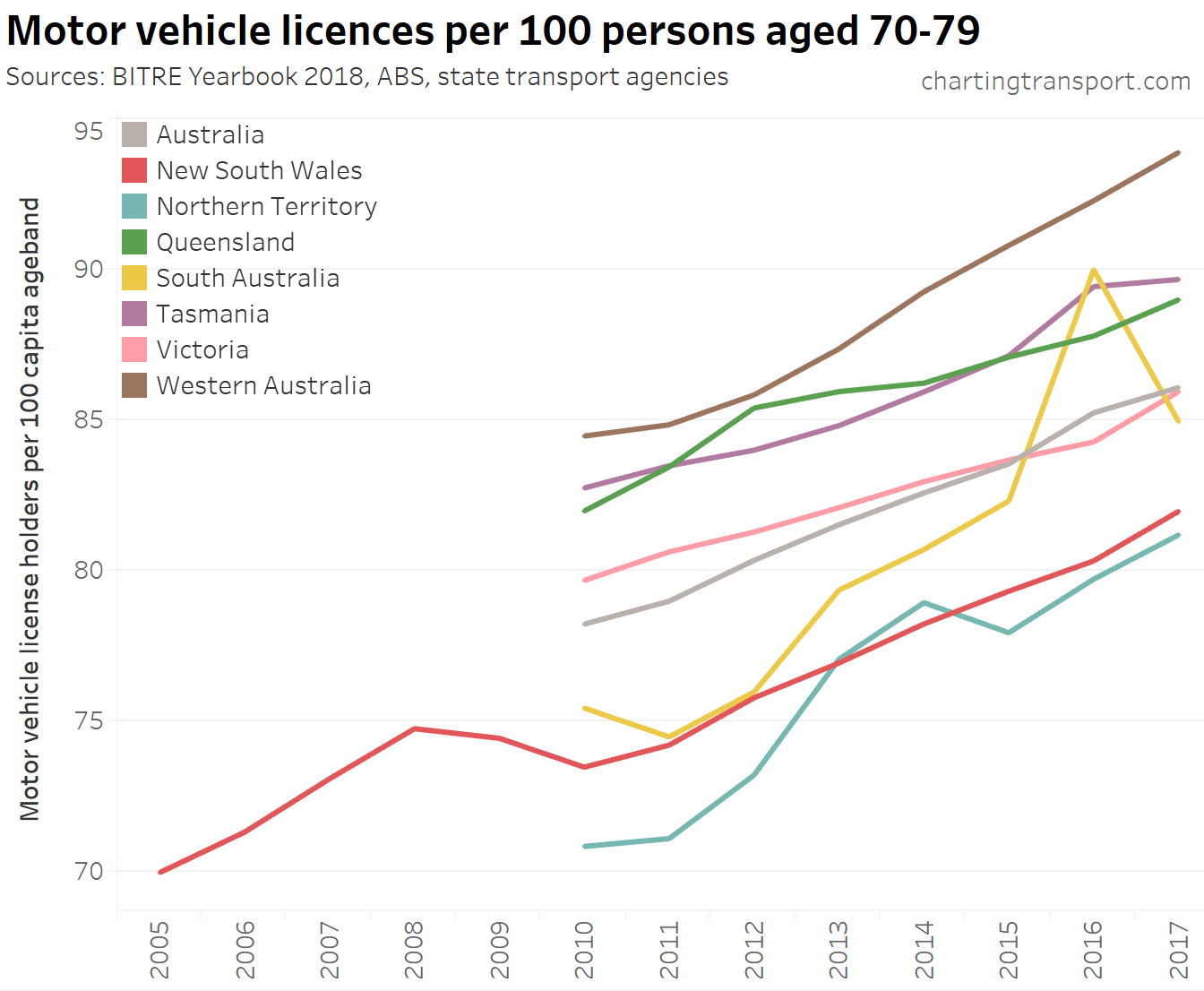

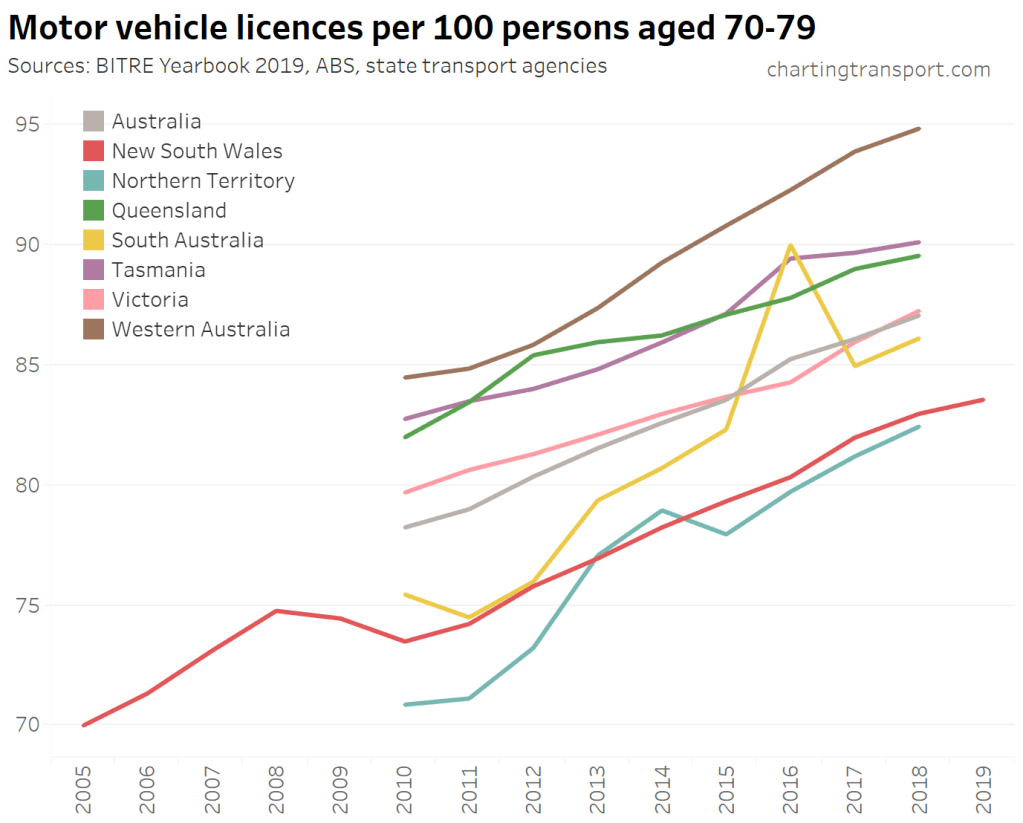

Licencing rates for people in their 70s are rising in all states (I suspect a data error for South Australia in 2016):

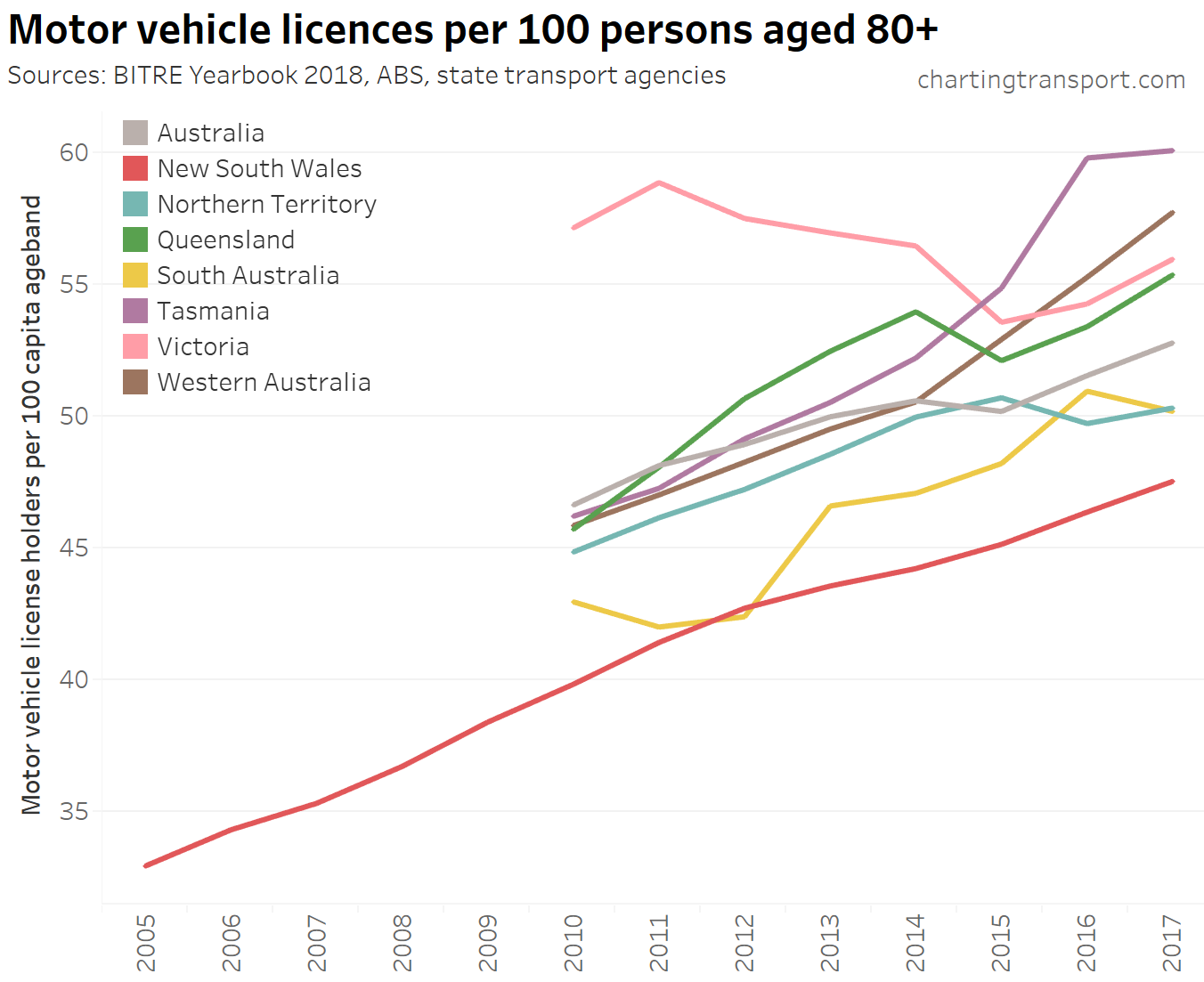

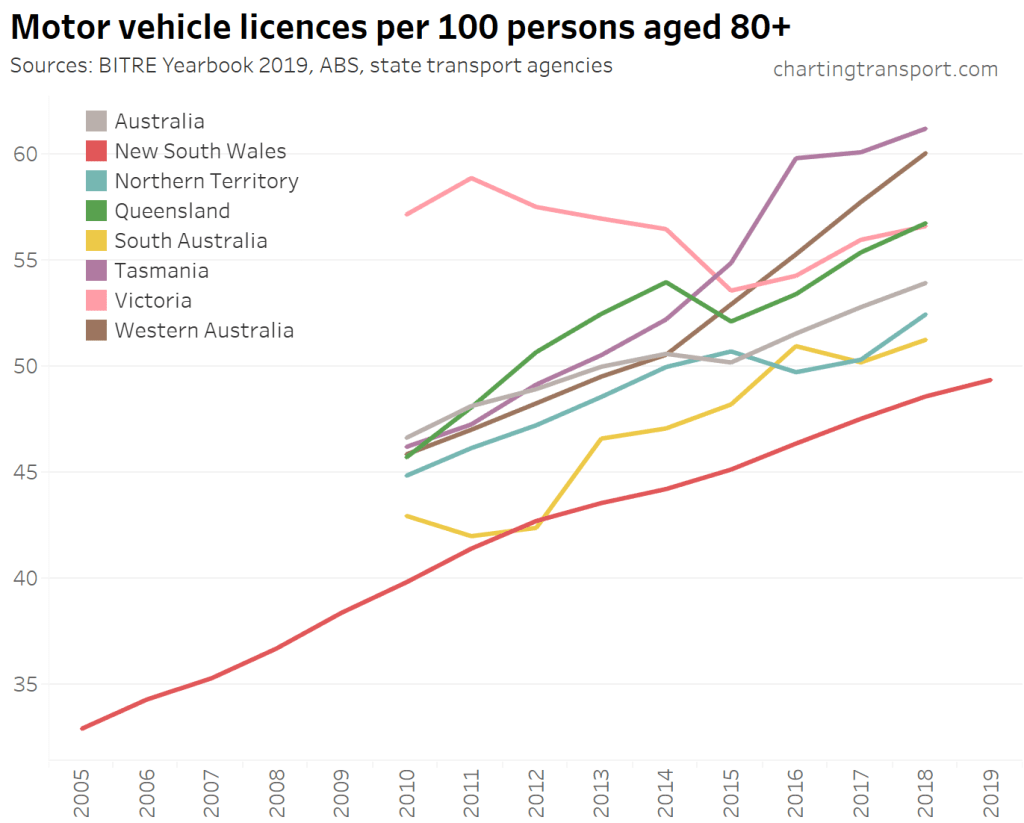

A similar trend is clear for people aged 80+ (Victoria was an anomaly before 2015):

See also an older post on driver’s licence ownership for more detailed analysis.

Transport greenhouse gas emissions

[this emissions section updated on 8 January 2020 with BITRE estimates for 1975-2019]

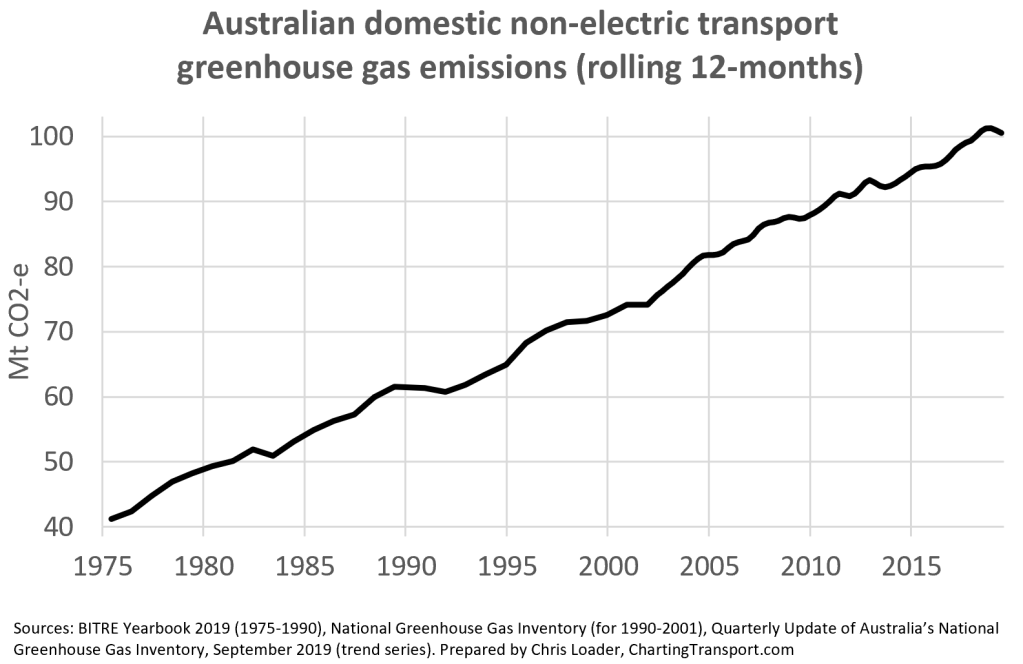

According to the latest adjusted quarterly figures, Australia’s domestic non-electric transport emissions peaked in 2018 and have been slightly declining in 2019, which reflects reduced consumption of petrol and diesel. However it is too early to know whether this is another temporary peak or long-term peak.

Non-electric transport emissions made up 18.8% of Australia’s total emissions as at September 2019.

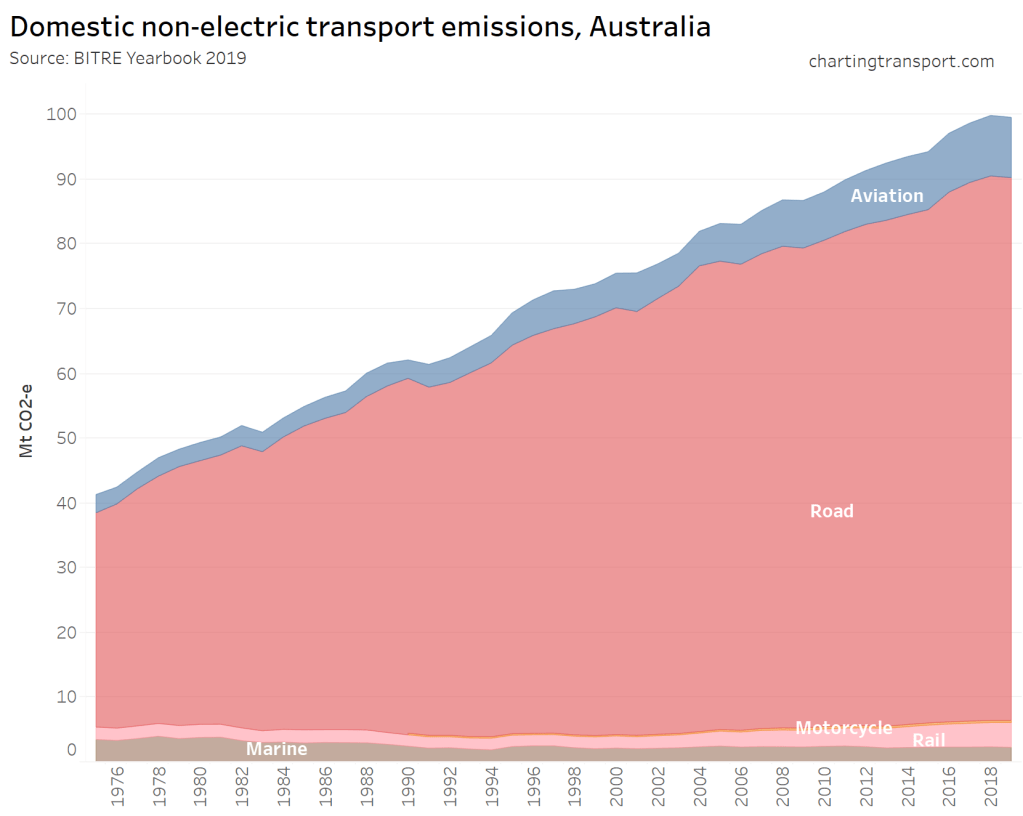

Here’s a breakdown of transport emissions:

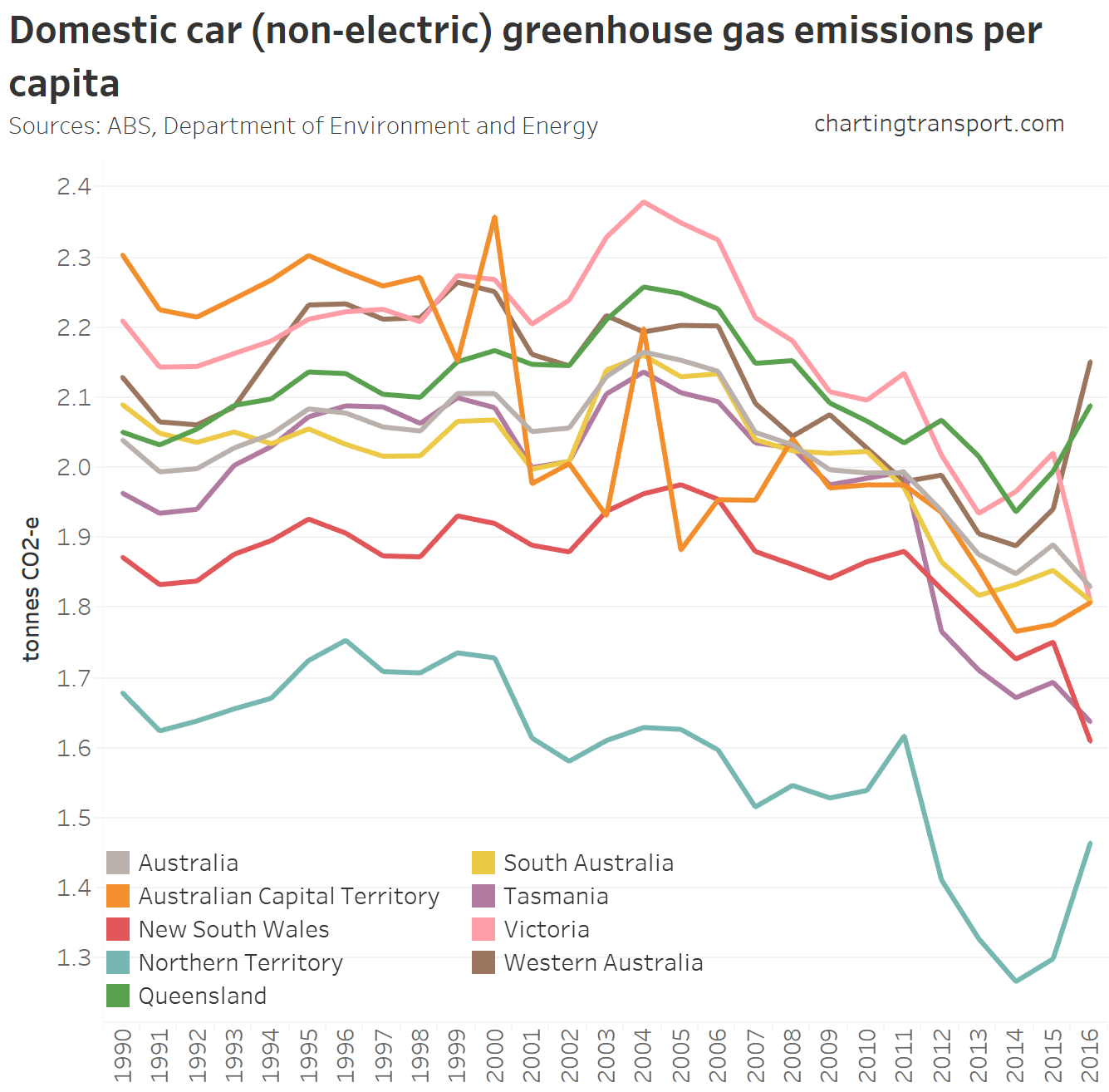

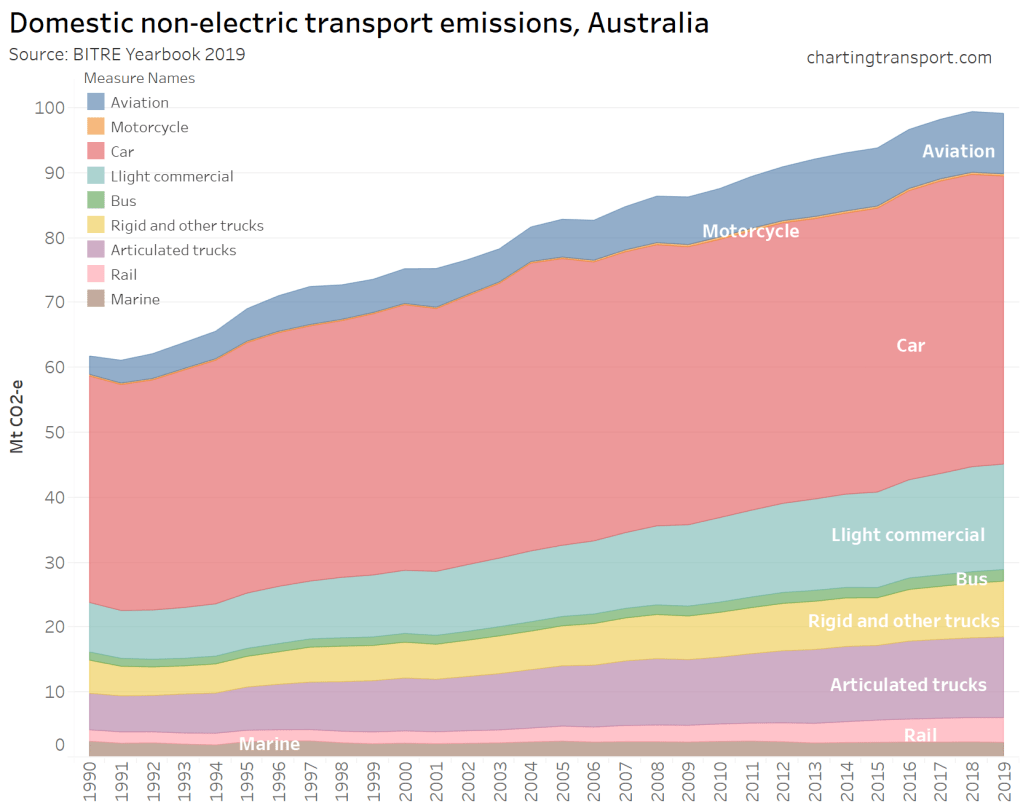

A more detailed breakdown of road transport emissions is available back to 1990:

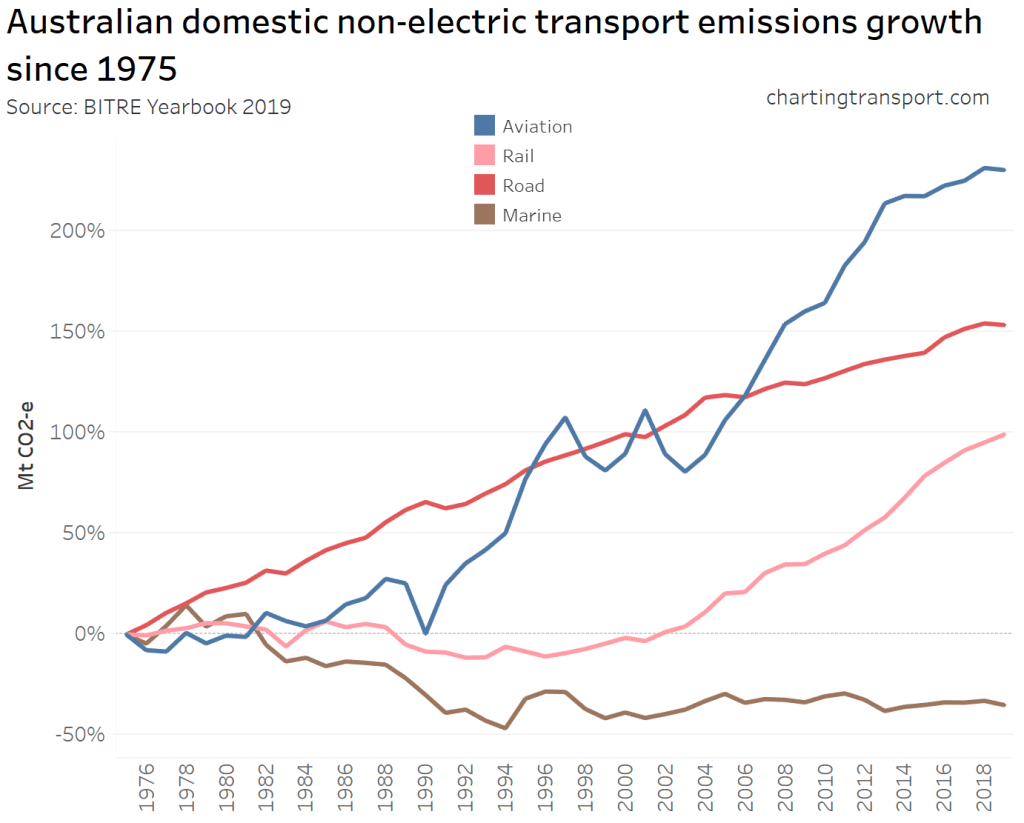

Here’s growth in transport sectors since 1975:

Road emissions have grown steadily, while aviation emissions took off around 1991. You can see that 1990 was a lull in aviation emissions, probably due to the pilots strike around that time.

In more recent years non-electric rail emissions have grown strongly. This will include a mix of freight transport and diesel passenger rail services – the most significant of which will be V/Line in Victoria, which have grown strongly in recent years (140% scheduled service kms growth between 2005 and 2019). Adelaide’s metropolitan passenger train network has run on diesel, but more recently has been transitioning to electric.

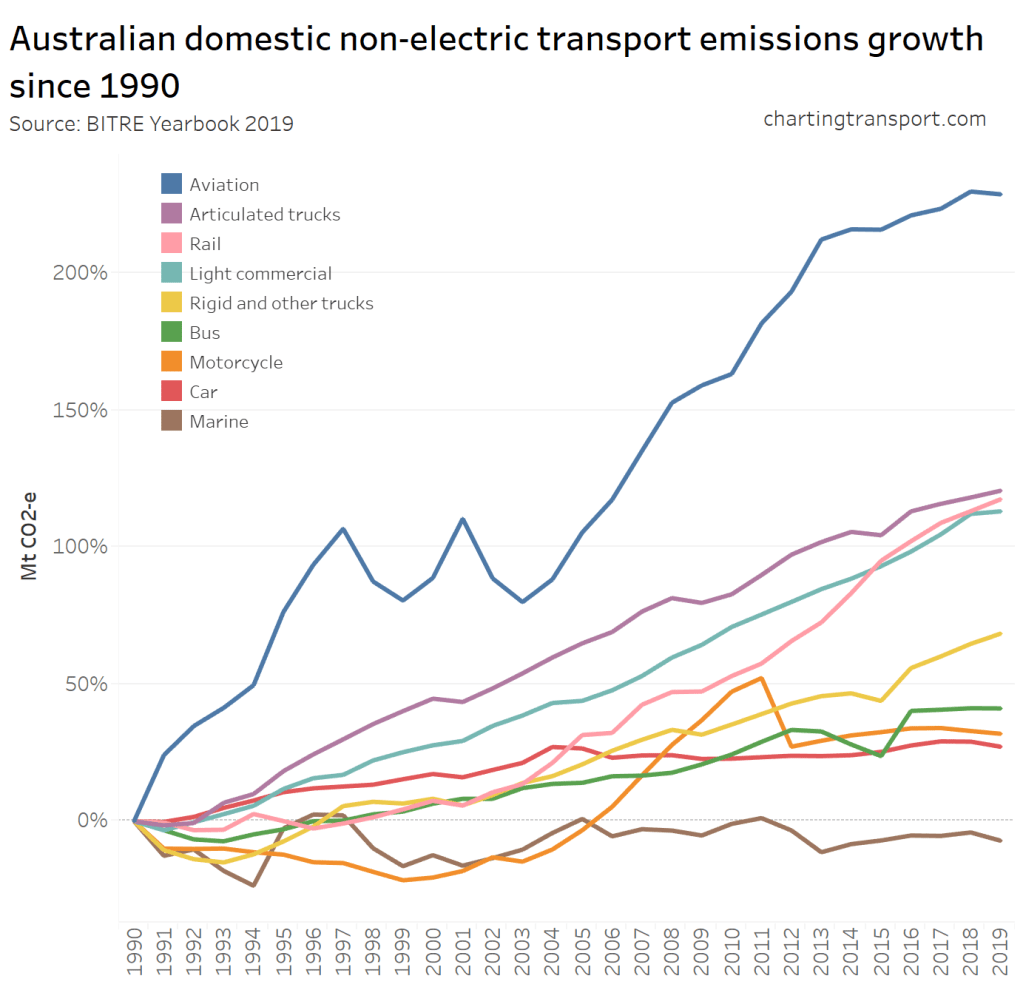

Here is the growth in each sector since 1990 (including a breakdown of road emissions):

Here are average emissions per capita for various transport modes in Australia, noting that I have used a log-scale on the Y-axis:

Per capita emissions are increasing for most modes, except cars. Total road transport emissions per capita peaked in 2004 (along with vehicle kms per capita, as above).

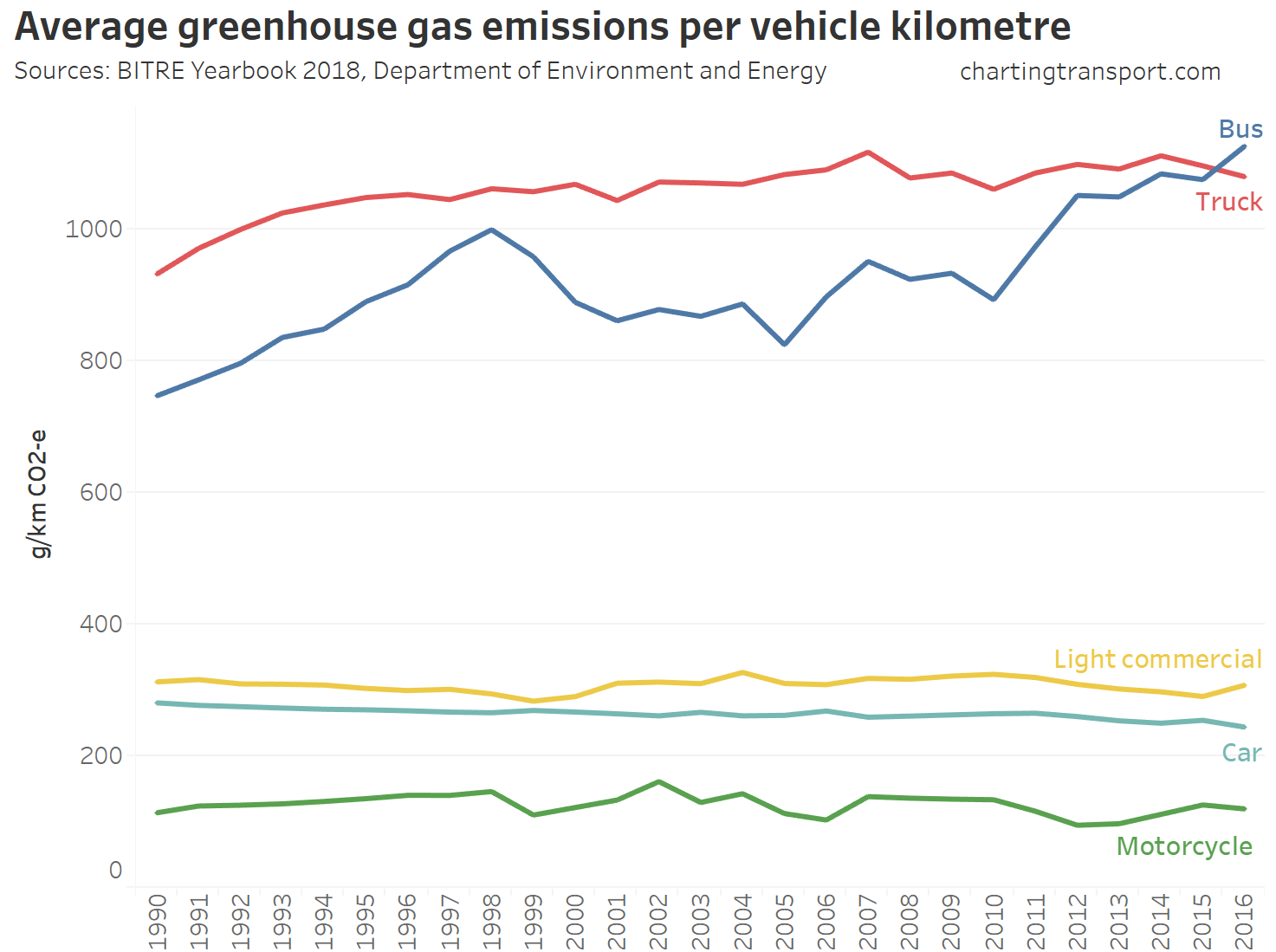

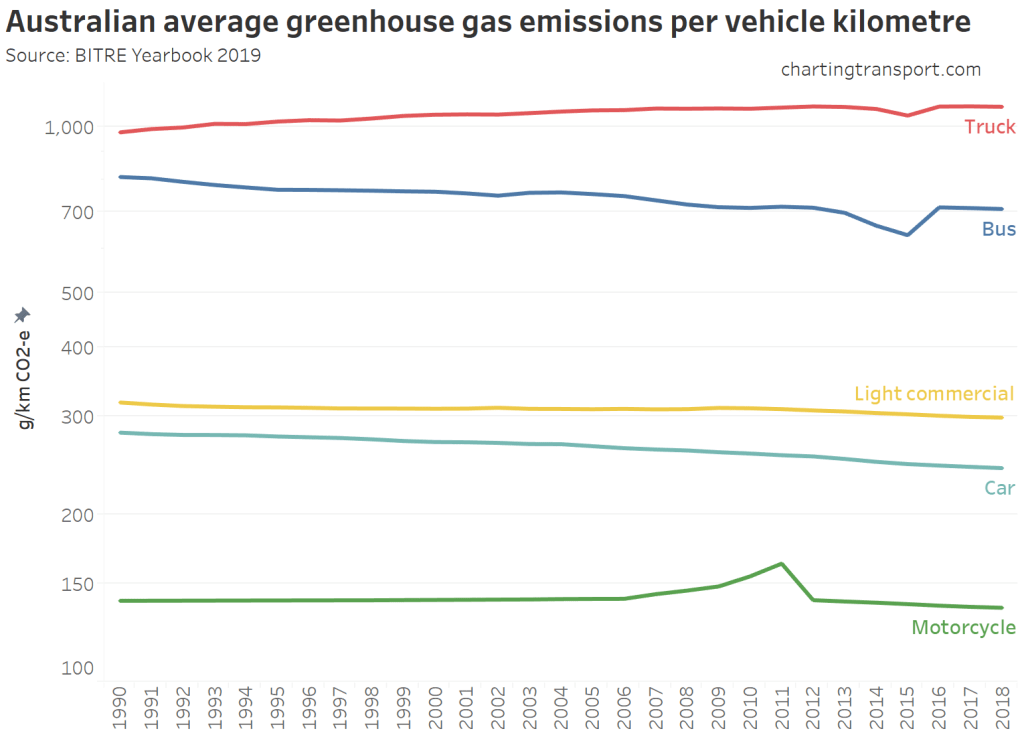

It’s possible to combine data sets to estimate average emissions per vehicle kilometre for different vehicle types (note I have again used a log-scale on the Y-axis):

Note: I suspect the kinks for buses and trucks in 2015, and motor cycles in 2011 are issues to do with assumptions made by BITRE, rather than actual changes.

The only mode showing significant change is cars – which have reduced from 281 g/km in 1990 to 243 g/km in 2019.

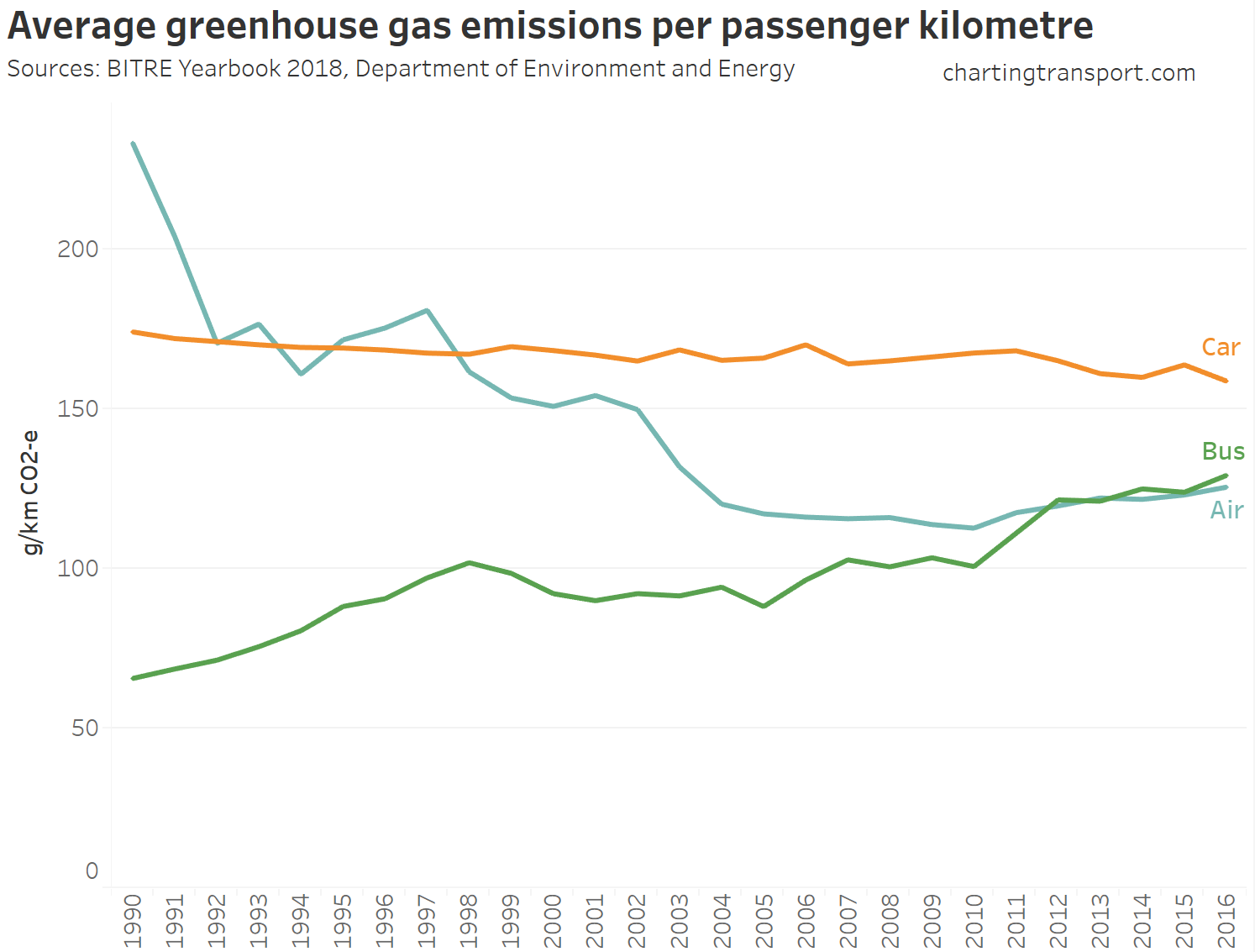

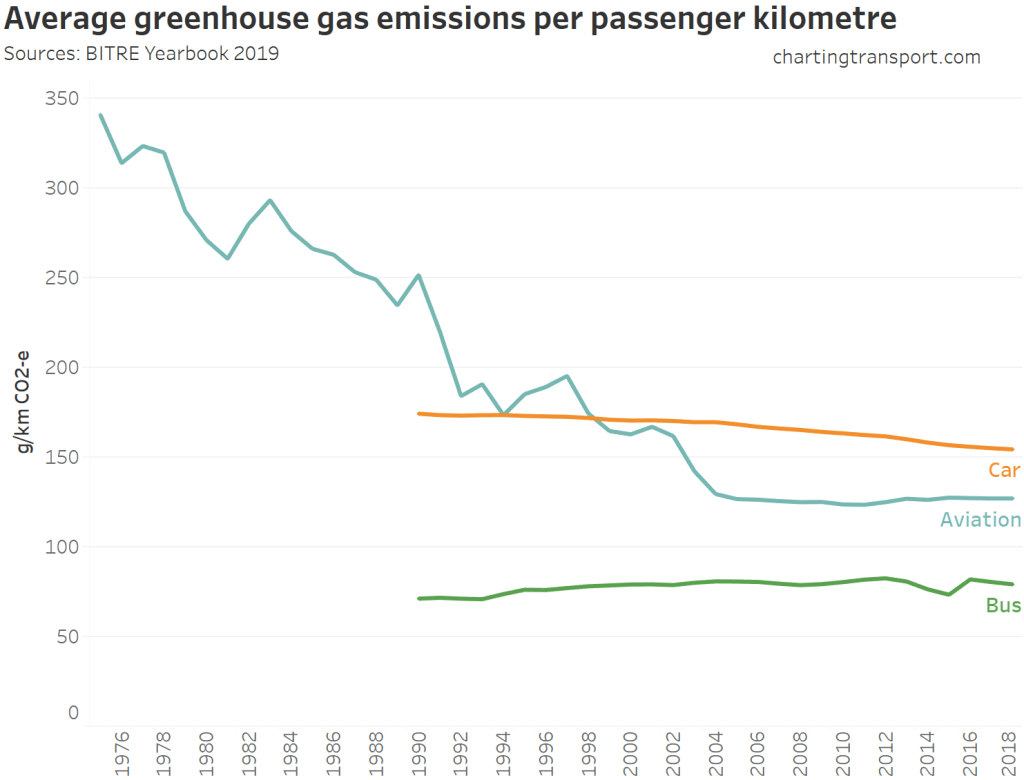

However, the above figures don’t take into account the average passenger occupancy of vehicles. To get around that we can calculate average emissions per passenger kilometre for the passenger-orientated modes:

Domestic aviation estimates go back to 1975, and you can see a dramatic decline between then and around 2004 – followed little change (even a rise in recent years). However I should mention that some of the domestic aviation emissions will be freight related, so the per passenger estimates might be a little high.

Car emissions per passenger km in 2018-19 were 154.5g/pkm, while bus was 79.4g/pkm and aviation 127.2g/pkm.

Of course the emissions per passenger kilometres of a bus or plane will depend on occupancy – a full aeroplane or bus will have likely have significantly lower emissions per passenger km. Indeed, the BITRE figures imply an average bus occupancy of around 9 people (typical bus capacity is around 60) – so a well loaded bus should have much lower emissions per passenger km. The operating environment (city v country) might also impact car and bus emissions. On the aviation side, BITRE report a domestic aviation average load factor of 78% in 2016-17.

Cost of transport

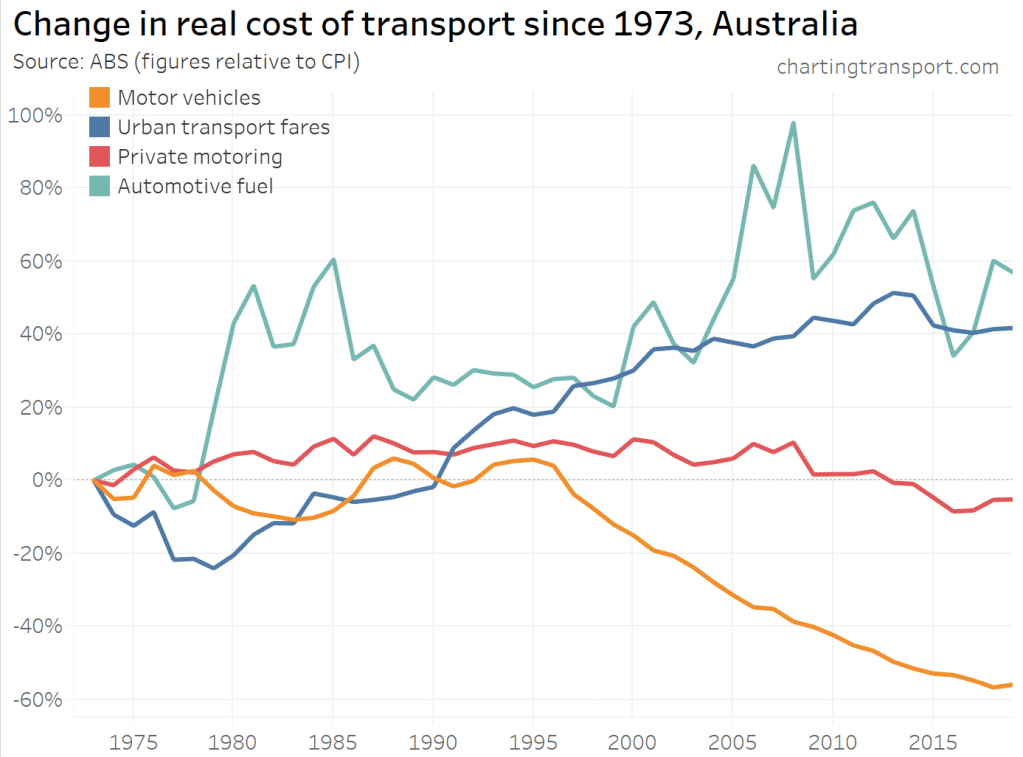

The final topic for this post is the real cost of transport. Here are headline real costs (relative to CPI) for Australia:

Technical note: Private motoring is a combination of factors, including motor vehicle retail prices and automotive fuel. Urban transport fares include public transport as well as taxi/ride-share.

The cost of private motoring has tracked relatively close to CPI, although it trended down between 2008 and 2016. The real cost of motor vehicles has plummeted since 1996. Urban transport fares have been increasing faster than CPI since the late 1970s, although they have grown slower than CPI (on aggregate) since 2013.

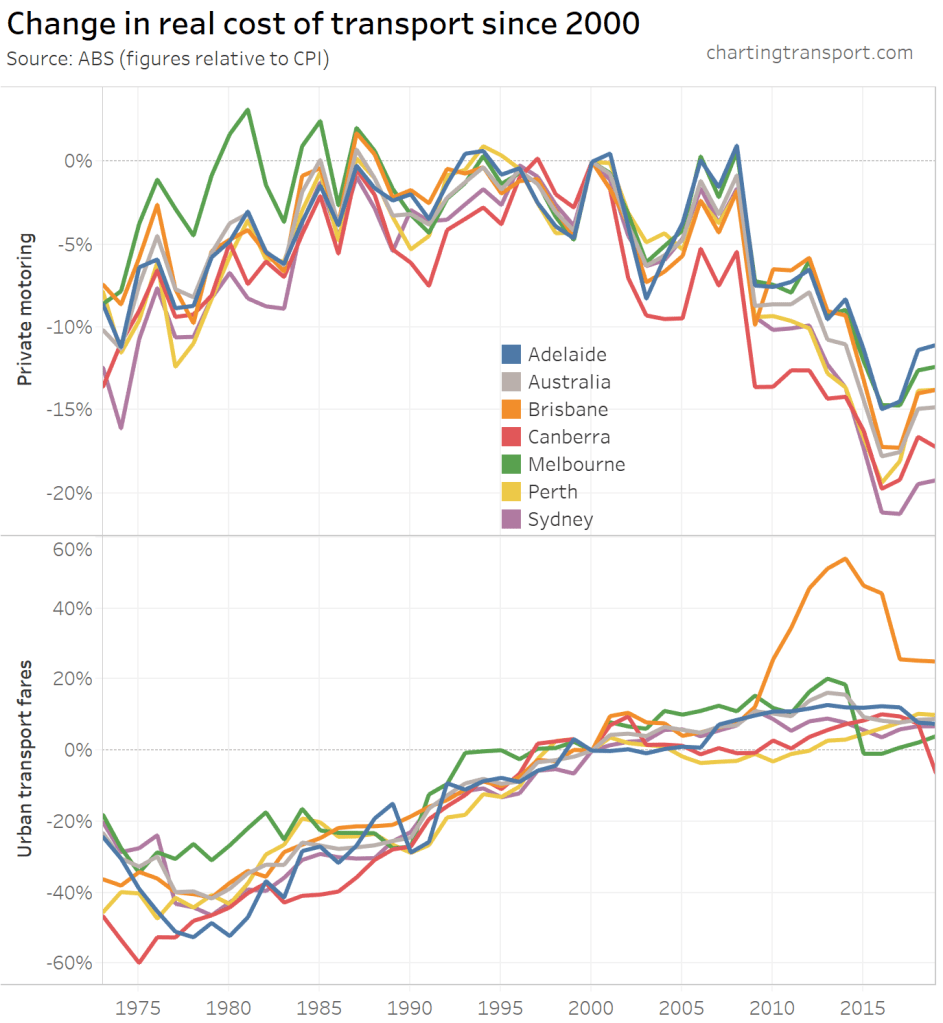

Here’s a breakdown of the real cost of private motoring and urban transport fares by city (note different Y-axis scales):

Note: I suspect there is some issue with the urban transport fares figure for Canberra in June 2019. The index values for March, June, and September 2019 were 116.3, 102.0, and 118.4 respectively.

Urban transport fares have grown the most in Brisbane, Perth and Canberra – relative to 1973.

However if you choose a different base year you get a different chart:

What’s most relevant is the relative change between years – eg. you can see Brisbane’s experiment with high urban transport fare growth between 2009 and 2017 in both charts.

Hopefully this post has provided some useful insights into transport trends in Australia.

Posted by chrisloader

Posted by chrisloader